It’s a damaging myth, and a surprisingly common one, that life insurance for a stay-at-home mum is an unnecessary expense. The truth is, the enormous financial value a mum provides is often completely overlooked, making this protection an absolute cornerstone of a family's financial security.

The key is to stop seeing the role as ‘unpaid’, and start seeing it for what it is: an essential economic engine powering the entire household.

Let's start by dismantling that common misconception right away. The idea that life insurance isn't a priority because a stay-at-home mum doesn't earn a traditional salary is fundamentally flawed. This perspective completely fails to recognise the immense economic contribution you make, every single day.

If your vital role were suddenly gone, your family would face immediate and significant costs to replace all the services you provide. Think of yourself as the 'Household CEO'. Your responsibilities stretch far beyond childcare, creating a complex support system that keeps the family running smoothly. If the worst were to happen, your partner would have no choice but to hire professionals to cover these duties, creating a huge and sudden financial strain.

To truly grasp the need for life insurance, we need to attach some real-world figures to these essential tasks. Suddenly, the household budget would need to stretch to cover things like:

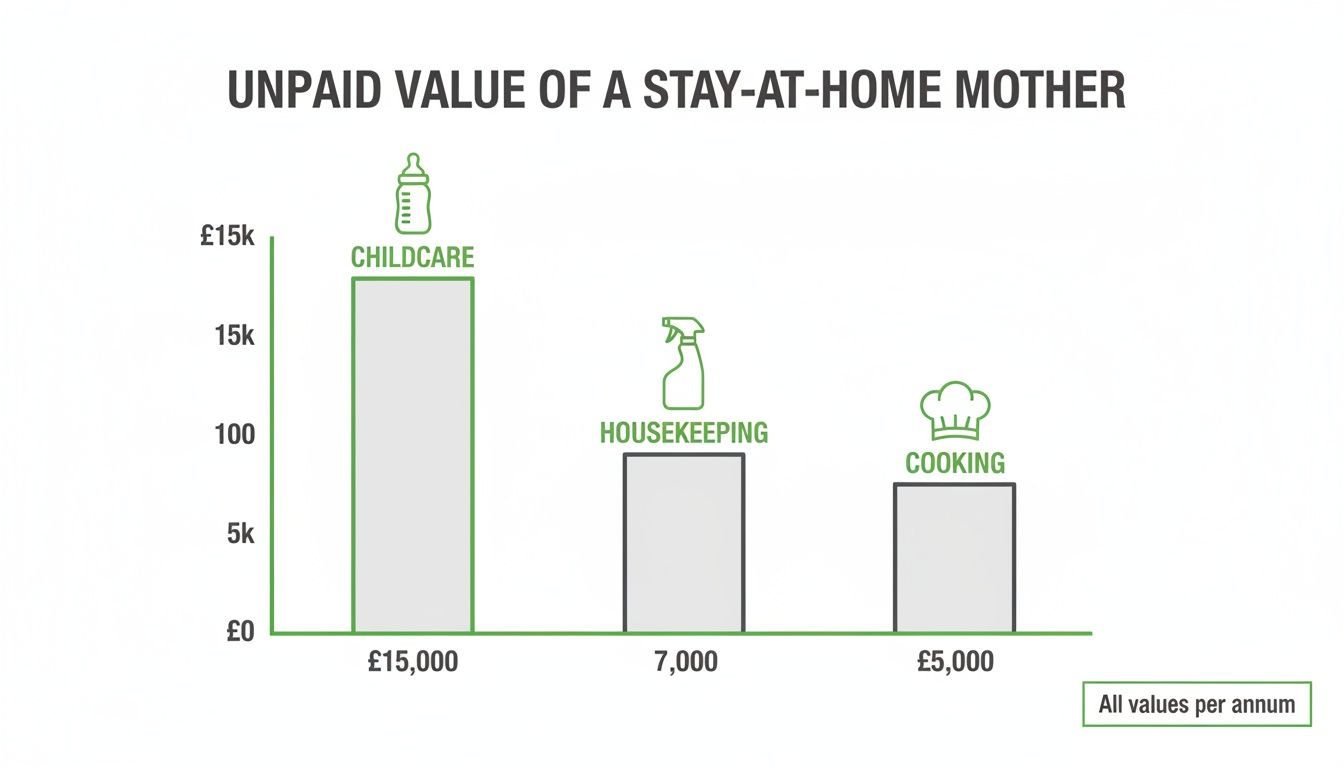

Let’s put some numbers on that. We’ve broken down the key roles a stay-at-home mum fulfils and provided estimated annual UK costs for outsourcing these services. This highlights the substantial financial gap your absence would create.

| Role/Service | Estimated Annual UK Cost |

|---|---|

| Childcare (Nursery/Nanny) | £14,000 - £20,000+ |

| Housekeeping/Cleaning | £4,000 - £6,000 |

| Cooking/Meal Preparation | £3,000 - £5,000 |

| Family Taxi Service | £2,000 - £3,000 |

Even a quick glance at the table shows how the costs would stack up, creating immense pressure on any family's budget.

This infographic breaks down the estimated annual costs for just three of the core responsibilities.

As the chart illustrates, the combined annual cost to replace just these basic services can easily exceed £27,000 a year. This isn't just about losing an income; it's about a massive new expense appearing overnight.

A life insurance policy for a stay-at-home mum doesn’t replace an income. It provides the funds necessary to pay for all the critical services she provided, ensuring the family remains financially stable during an incredibly difficult time.

A payout from a life insurance policy, like an affordable term life insurance plan , acts as a financial buffer. It gives your family the resources to grieve without the added, crushing stress of financial collapse.

It’s not just an insurance policy. It’s a safety net for your children’s future.

Now you’ve seen the powerful financial reasons for getting cover, let’s get into the ‘what’. Dipping your toe into the world of life insurance can feel a bit overwhelming, but for a stay-at-home mum, the choices are usually pretty straightforward. The key is simply to find a policy that lines up with your family’s needs and timeline.

The two most common and suitable options are Term Life Insurance and Whole of Life Insurance. They each do a different job, and getting your head around the distinction is the first step towards choosing with confidence. Let's break down how they work in simple terms.

Think of Term Life Insurance as a large, protective umbrella you put up to shield your family during a specific period—typically while your children are young and totally reliant on you. This is by far the most popular choice for families looking for life insurance for stay-at-home mums, mainly because it’s both affordable and incredibly practical.

You choose a set period, or ‘term’—say, 20 years—designed to last until your youngest child is financially independent. If you were to pass away within that term, the policy pays out a lump sum. If the term ends and you're still here, the cover simply stops, and so do your payments.

Its primary goal is crystal clear:

For most families, Term Life Insurance is the perfect fit. It offers substantial protection during the years your children need it most, at a cost-effective price that fits neatly into the family budget.

In contrast, Whole of Life Insurance does exactly what its name suggests: it covers you for your entire life. As long as you keep up with the premiums, a payout is guaranteed, no matter when you pass away. Because of that guarantee, it costs more than term cover.

This type of policy is less about replacing your immediate economic value and more about long-term financial planning. A stay-at-home mum might consider it to:

Finally, let’s talk about Critical Illness Cover. This isn't a standalone life insurance policy but a powerful add-on. It pays out a tax-free lump sum if you are diagnosed with a serious, specified illness like cancer, a stroke, or a heart attack.

For a stay-at-home mum, a serious illness can be just as financially devastating as a death. The payout could give your partner the funds to take time off work, pay for specialist medical care, or hire extra help around the house. It's an extra layer of security that provides real peace of mind when you need it most.

Figuring out the right amount of cover can feel like pulling a number out of thin air, but it’s far more straightforward than you might think. There’s no single magic figure that fits every family, but there is a simple logic you can follow to land on a sum that provides genuine security.

The goal is to work out a lump sum that could replace the financial value you bring and clear any major debts, giving your family a stable foundation to rebuild from. A good rule of thumb for life insurance for stay at home mums is to aim for enough cover to see your youngest child through to financial independence, usually around age 18 or 21.

You don’t need a complicated financial spreadsheet to get started. Just think about the biggest financial hurdles your family would face if you were suddenly no longer there.

Your calculation should cover three core areas:

A common starting point recommended by financial experts is to get between £250,000 and £400,000 of cover. This range often provides enough funds to clear a typical mortgage and cover childcare costs for several years, acting as a strong financial safety net.

Let's make this real with a quick example. Imagine a family with two children, aged two and five, and an outstanding mortgage of £150,000.

Adding these up gives a target cover amount of £370,000. This simple calculation transforms an abstract worry into a clear, manageable figure. It’s not about replacing you—that's impossible—but it is about providing the financial stability your family would desperately need.

Choosing your cover amount is a huge step, but it’s only half the story. How you actually structure the policy is just as important, as it determines how quickly and effectively your loved ones get the money.

These details are easy to overlook, but getting them right makes all the difference. Let’s walk through the key decisions you'll need to make, starting with whether you and your partner should share a policy or have one each.

When you’re looking at life insurance as a couple, you’ll come across two main ways to set things up:

While two single policies might cost a fraction more each month, the potential for a dual payout provides much more comprehensive protection. It’s why so many families prefer to go down this route.

Now for what is arguably the single most important step you can take when arranging your life insurance for stay at home mums. Writing your policy in trust is a simple, completely free process that offers massive advantages for your family.

Think of a trust as a ‘VIP pass’ for your life insurance payout. Without one, the money becomes part of your legal estate. It gets tangled up in a lengthy legal process called probate, which can drag on for months, and the payout could even get hit by Inheritance Tax.

By placing your policy in trust, the payout completely bypasses your estate and goes directly to your chosen beneficiaries. Your family gets the money they desperately need much faster—often within weeks instead of months—and the full amount is shielded from a potential 40% Inheritance Tax bill.

This simple bit of paperwork ensures your financial safety net works exactly as intended: quickly, efficiently, and without any unnecessary deductions or delays. It's a non-negotiable step for maximising your family's protection.

When you apply for a policy, insurers carry out a process called underwriting. It might sound a bit technical, but it’s really just their way of working out how much your monthly premiums will be.

It’s not some mysterious black box; it's simply an assessment of risk based on a few key personal details. Getting your head around these factors helps you see exactly why getting cover locked in sooner rather than later is often the smartest move you can make.

The main things that influence your price are straightforward and logical. Insurers will look at your age, your current health, and any pre-existing medical conditions you might have. They’ll also take into account lifestyle choices, like whether you smoke or vape, as this has a direct impact on life expectancy.

Of course, the specifics of the policy itself play a huge role, too. The amount of cover you choose and how long you want it for will directly affect the cost. A bigger payout or a longer-running policy will naturally mean higher premiums.

To put it simply, insurers are trying to build a clear picture of your overall health and the level of cover you need. The most significant factors include:

It's vital to be completely transparent during your application. While it might be tempting to omit a detail to get a lower price, this can have serious consequences. Insurers have a strong track record of paying claims, but non-disclosure is one of the few reasons a claim might be rejected.

Fortunately, the vast majority of families get the support they expect when they need it most. In fact, research shows that 96.7% of new life insurance claims in the UK were paid out in 2023, giving thousands of families enormous peace of mind.

Feeling ready to secure your family’s future? Good. Taking that next step is much more straightforward than you might think. This guide has hopefully armed you with the confidence to work out how much cover you need and understand how the different policies work. Now, let’s turn that knowledge into a plan of action.

The process is actually very simple and really just boils down to a couple of key actions. First, use what you've learned here to decide on a target amount of cover. Think about your mortgage, future childcare costs, and day-to-day expenses to land on a figure that feels right for your family's unique situation.

Next, just pull together some basic personal details—things like your age, a quick overview of your health, and a few lifestyle details. With that ready, you’re in the perfect position to start comparing quotes. Using a free, independent comparison service like Life Cover Plans is easily the most efficient way to see what leading UK insurers can offer you.

This approach saves you the hassle of filling out endless forms on different websites. Instead, one secure form connects you with expert advisors who can provide tailored, no-obligation quotes from trusted providers. This is your most direct route to finding affordable and robust life insurance for stay at home mums. You can also find out more about the different policy types in our detailed guide on whole of life insurance.

Taking this step is so important, especially when you learn that nearly half of UK mums have no protection at all. Research has shown that a shocking 46% of mothers currently have no life insurance policy in place—a worrying statistic given the vital economic role they play.

By comparing quotes, you make sure you get the right protection at the best possible price. It’s a simple action that delivers lasting peace of mind for you and your family.

It's completely normal to have a few specific questions buzzing around as you look into life insurance. This section tackles some of the most common queries we hear from stay-at-home mums, giving you the clear, straightforward answers you need to feel confident.

Yes, absolutely. You can definitely apply for life insurance while you're pregnant, and insurers handle these applications every single day.

It's worth knowing, however, that certain pregnancy-related health issues, like gestational diabetes, could have an impact. In some cases, an insurer might choose to postpone a final decision until after your baby arrives. The best advice is always to apply as early as you can and be completely open and honest on your application.

One of the huge benefits of life insurance is that the payout is generally paid to your family completely tax-free.

But there's one important catch. If the policy isn't set up correctly, the money could be considered part of your legal estate. This means it might be hit by Inheritance Tax (IHT) if the total value of your estate goes over the current threshold. The solution is simple: write your policy in trust. This is an easy and incredibly effective way to make sure the money goes straight to your loved ones without getting tangled up in your estate for tax purposes.

Putting your policy in trust is like creating a protective financial wrapper around it. It ensures your family gets the full amount, quickly, and shields it from a potential 40% Inheritance Tax bill. It’s an essential step to maximise their security.

If you ever find yourself struggling to keep up with your premiums, the most important thing is not to panic and let the policy cancel. Your first move should be to get in touch with your insurer or financial advisor straight away, as you have several options.

You might be able to reduce your amount of cover, which would lower your monthly payments to something more manageable. Some policies also have a feature called a 'waiver of premium'. This is a valuable add-on that covers your payments for you if you become seriously ill or injured and can't work. The key is to act before you miss a payment—a lapsed policy means your family loses that vital protection entirely.

Ready to secure your family's future with total peace of mind? At Life Cover Plans, we make it simple to compare tailored, no-obligation quotes from the UK's leading insurers. Take the first step towards securing your family's future, click below to get your free quote now!

Get My Free Quote >>