Becoming a parent changes your perspective on just about everything. Suddenly, your main job is to make sure your kids have the best possible future, and the most direct way to do that is with life insurance for parents. It’s a policy designed to pay out a tax-free lump sum if you’re no longer there to provide for them. Think of it less as a financial product and more as a foundational act of love and responsibility.

Thinking about life insurance isn't about dwelling on the worst-case scenario. It’s actually a powerful and practical step towards building a wall of financial protection around the people who matter most. It’s the ultimate backup plan, making sure your family’s dreams and opportunities don’t disappear if you do.

Picture a young family, Mark and Sarah, with two small children. They’ve just bought their first home and are juggling nursery fees, bills, and trying to save for the future. Their biggest asset is their ability to earn an income, but their biggest liability is the mortgage.

If something were to happen to one of them, the surviving partner would face an immense emotional and financial burden all at once. This is exactly where life insurance steps in to act as a safety net.

A life insurance policy provides a tax-free cash payout that can cover huge financial obligations, removing a massive source of stress during an already difficult time. This lump sum can be used for whatever the family needs to maintain their quality of life, including:

A life insurance payout gives your family breathing room. It ensures that money is the last thing they have to worry about, allowing them to focus on grieving and rebuilding their lives together.

This peace of mind is why so many UK parents make this kind of protection a priority. Recent data from Q1 showed 452,799 retail investment sales, which generated a massive £13.85 billion in total premium amounts. This reflects a deep commitment from parents to safeguard their families’ futures. You can explore more about these life insurance sales trends to get a feel for the market. For Mark and Sarah, a simple policy transforms their biggest "what if" into a reassuring "even if," knowing their children's futures are secure.

Navigating the world of life insurance can feel like learning a new language, but when you boil it down, you're really only looking at a few core options. Getting your head around these choices is the first step to finding a policy that fits your family's unique situation perfectly. The main decision you'll face is whether you need cover for a specific chunk of time, or for the rest of your life.

Think of it this way: are you building a temporary financial bridge to get your kids safely to the other side of childhood, or are you creating a permanent monument to leave behind as a legacy? Each approach has its own purpose, and the right one for you depends entirely on what you want that safety net to achieve.

This simple flowchart can help you visualise the thought process for parents weighing up their life insurance needs.

As the chart shows, the journey from spotting a need to getting a quote is a straightforward path, designed to bring clarity and a bit of peace of mind.

To help you match your family’s needs to the right type of cover, this quick comparison table breaks down the main options at a glance.

| Policy Type | Best For | Typical Payout Trigger | Key Benefit |

|---|---|---|---|

| Term Life Insurance | Covering debts like a mortgage and replacing income while children are young. | Death occurring within a pre-agreed policy term (e.g., 25 years). | High level of cover for an affordable monthly premium. |

| Whole of Life Insurance | Leaving a guaranteed inheritance, covering funeral costs, or settling an Inheritance Tax bill. | Death occurring at any point in the future. | A guaranteed payout, no matter when you pass away. |

| Critical Illness Cover | Protecting your finances against the impact of a serious illness that stops you from working. | Diagnosis of a specific, serious medical condition listed in the policy. | A 'living benefit' that pays out while you're still alive to aid recovery. |

Each policy is a different tool for a different job. The key is to pick the one that solves the specific financial problem you're worried about.

Term life insurance is, without a doubt, the most popular choice for parents, and for good reason. It’s straightforward, affordable, and perfectly designed to protect your family during their most financially vulnerable years.

Imagine it as a safety net stretched out for a specific period, or ‘term’—typically between 10 and 30 years. You choose this term to line up with major life events, like the years until your mortgage is paid off or until your youngest child has flown the nest. If you were to pass away within that term, your family receives a tax-free lump sum. If you outlive it, the policy simply expires.

Within this category, there are two main flavours you’ll come across.

This is the simplest form of cover. Both the payout amount (the sum assured) and your monthly payments (the premiums) are locked in and stay the same for the entire policy term. If you take out a £250,000 policy for 25 years, your family would get £250,000 whether you passed away in year one or year 24.

Best for: Covering general living costs, childcare, and future education expenses. Its predictability makes it ideal for parents who want a consistent, reliable level of protection.

With this type of policy, the potential payout gets smaller over time, usually in line with a repayment mortgage. Because the insurer's potential payout reduces each year, the premiums are typically lower than for level term cover.

Best for: Specifically covering a large repayment debt like a mortgage. It’s designed to make sure your biggest liability is cleared without leaving your family out of pocket.

You can learn more about the specifics in our guide on term life insurance policies and how they protect your family.

In contrast to term insurance, whole of life insurance is designed to provide a payout no matter when you pass away, as long as you keep paying the premiums. Think of it less as a temporary safety net and more as a guaranteed financial gift for your loved ones.

Because the payout is certain, these policies are more expensive. They are often used for specific financial planning goals rather than just covering short-term debts and childcare costs.

A whole of life policy is a powerful tool for legacy planning. It ensures there is a definite sum available to cover funeral costs, settle an inheritance tax bill, or simply leave a meaningful inheritance for your children or grandchildren.

This type of cover is a permanent fixture in your financial plan, offering peace of mind that there will be a payout regardless of how long you live.

What happens if you don't pass away but are diagnosed with a serious illness that stops you from working? This is where Critical Illness Cover comes in. It's usually offered as an optional add-on to most life insurance policies.

This cover pays out a tax-free lump sum if you are diagnosed with one of the specific serious conditions listed in the policy, such as some types of cancer, a heart attack, or a stroke. This money can be a real lifeline, helping you to:

Adding this cover provides a crucial financial buffer against the unexpected, protecting your family’s financial stability not just in the event of death, but also during a serious health crisis. It ensures your focus can be on recovery, not on money worries.

Figuring out the right amount of life insurance can feel a bit like guesswork, but it’s far more of a science than an art. There's no single "magic number" that works for every family. The right figure is deeply personal, built entirely around your unique circumstances, your debts, and the future you want for your children.

The goal isn’t just to pick a big number out of thin air; it’s to land on a precise sum that would allow your family to carry on with their lives without any financial turmoil. Think of it as creating a financial blueprint for their future, one that's robust enough to cover all the big obligations and aspirations you have for them.

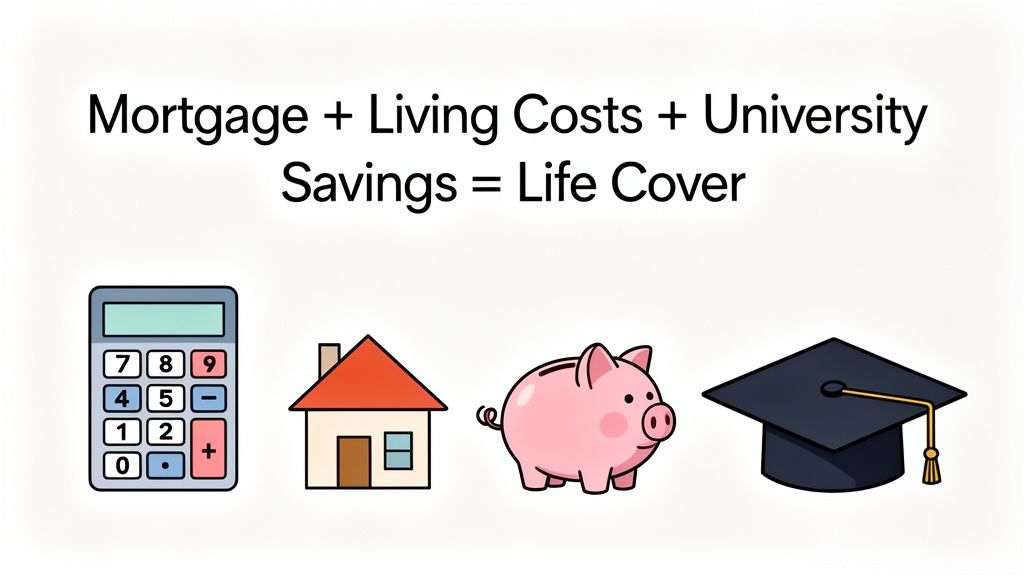

To work out a realistic figure, you can use a pretty straightforward formula. The idea is to simply add up all your major financial responsibilities and any big costs you see on the horizon. This gives you a clear and logical target for your life insurance for parents policy.

Start by looking at these key areas:

Your Total Cover = (Mortgage + Other Debts) + (Annual Living Costs x Years Until Children Are Independent) + (Major Future Costs)

This framework gives you a solid, evidence-based number to work with, turning a vague guess into a calculated strategy. It’s a logical way to make sure nothing important gets overlooked. For a deeper look into protecting your largest debt, our guide on mortgage life insurance is a great resource.

Let's imagine a family: Alex and Ben, both 35, with two children aged 3 and 5. They want to be sure their family is protected until their youngest finishes university at 21, so they're looking for cover for the next 18 years.

Here’s how they might break down their numbers:

Their first calculation comes to £780,000 (£190k + £540k + £50k). It sounds like a massive sum, but it's important to remember that policies offering this level of cover can be surprisingly affordable, especially when you're young and in good health.

Once you have your initial estimate, there are a couple of final adjustments worth making. First, take into account any protection you might already have, like a death-in-service benefit from your employer. This often pays out a multiple of your salary and can significantly reduce the amount of personal cover you need to buy.

You should also think about the long-term impact of inflation, which can chip away at the real value of your payout over time. You might want to consider an 'increasing' term policy, where the sum assured rises each year to keep pace with the cost of living.

Finally, you can take comfort in just how stable the UK insurance industry is. The sector maintains exceptional financial strength, with firms holding an aggregate Solvency Capital Requirement (SCR) coverage ratio of 185%. This high level of security means you can be confident that insurers have more than enough resources to meet their promises. This robust foundation provides the ultimate peace of mind when you're planning for your family's future.

Lots of parents are pleasantly surprised when they find out how affordable life insurance can actually be. It’s easy to imagine a massive monthly bill, but for most people, that’s just not the reality. The cost isn’t some random number plucked from thin air; it’s calculated by logically assessing risk, which means your personal circumstances are what shape the price you pay.

This is actually great news. It means you’re not in the dark about the costs, and it gives you a bit of control. By understanding the main factors at play, you can see the pricing process not as a hurdle, but as a clear path to getting the right protection for your family without breaking the bank.

Insurers in the UK look at a handful of key details to figure out the likelihood of having to pay out a claim. It's pretty simple: the lower they see the risk, the lower your monthly premium will be.

Here are the main things they’ll look at:

The most important takeaway is that getting life insurance for parents earlier is almost always cheaper. Securing a policy in your 30s, when you're likely to be in good health, can lock in a low rate for decades to come.

So, what does all this look like in the real world? The idea that you need a huge budget for decent cover is one of the biggest myths out there. For a healthy person, you can often get a substantial amount of protection for less than the price of a few weekly coffees or a Netflix subscription.

This is especially true if you also want to protect your family from the financial fallout of a serious health issue. You can find out more about how this works by reading our guide to life insurance with critical illness cover, which provides a payout if you're diagnosed with a specified condition.

To give you a clearer picture, let's look at some real-world examples for a healthy, non-smoking parent aged 35.

This table shows just how much cover you can get for a surprisingly small monthly outlay.

| Monthly Premium | Example Level Term Cover Amount (£) | Term Length |

|---|---|---|

| ~£6 per month | £100,000 | 25 years |

| ~£10 per month | £250,000 | 25 years |

| ~£18 per month | £500,000 | 25 years |

As you can see, even a policy providing a £250,000 tax-free payout—enough to clear a big chunk of the mortgage and leave a significant buffer—can be incredibly affordable. This is exactly why it’s so important to get a personalised quote based on your own details instead of just assuming it will be out of reach. When it comes to buying life insurance, your age and health are your greatest assets.

Finding the best life insurance for parents used to be a long, drawn-out affair, but these days you can sort the whole thing out from the comfort of your own home. Using an online comparison service is the modern way to get a crystal-clear view of your options, making sure you find the right protection at the best possible price.

The whole process is designed to be refreshingly simple. It kicks off with you plugging in a few basic details about yourself and the amount of cover you have in mind. This first step is quick and gives the system everything it needs to pull quotes from a wide range of top UK insurers, all in one go.

Before you dive in, it’s a good idea to have a few key details to hand. This will make the online form even quicker to whizz through and ensures the quotes you get back are as accurate as they can be.

You'll generally need:

Once you pop these details into a single secure form, you can see multiple quotes almost instantly. It saves you the hassle of trekking around to each insurer one by one.

After you’ve had a look at your initial quotes, the next step usually involves a quick chat with an FCA-authorised advisor. This is a hugely valuable part of the process. They aren't just there to sell you a policy; their job is to make absolutely certain the cover you’ve chosen is a perfect fit for your family.

An expert advisor can take a look at your situation, answer any specific questions you have, and help you fine-tune the details. This makes sure you're not paying for features you don't need, and that there are no gaps in your family’s financial safety net.

This conversation is completely free and comes with no obligation whatsoever. It’s just a professional check to give you total confidence in your decision before you commit. It’s the crucial step that turns a list of prices into a policy that truly works for you and your family.

The UK life insurance market is buzzing with activity, and the intense competition between insurers drives real value for customers. This competitive landscape, combined with strong regulation, means parents can make informed decisions with confidence. You can discover more insights about the UK insurance market and see how it works in your favour.

Once you’re happy with your chosen policy and have had that chat with an advisor, you can finalise the application. The insurer will review your details, and in many cases, your cover can be put in place very quickly. The whole journey, from getting your first quote to being fully covered, can often be wrapped up in under an hour. It’s a simple, effective way to lock in that vital financial protection for your family.

Once you've got your life insurance sorted, there's one simple but incredibly powerful final step that so many parents miss: placing your policy in trust. It might sound a bit technical, but it’s actually a straightforward process that makes sure your financial safety net works exactly as you intended, right when your family needs it most.

Think of a trust as an express delivery service for your life insurance payout. Normally, when someone passes away, their assets get bundled into their estate and have to go through a lengthy legal process called probate. This can drag on for months, sometimes even years, leaving your family waiting for the very funds you arranged to protect them.

Writing your policy in trust completely bypasses this delay. The money is paid directly to the people you choose (your trustees) to look after it for your children.

A trust is just a simple legal arrangement. When you place your life insurance for parents policy into one, you’re essentially creating a protective bubble around the payout. This separates it entirely from the rest of your personal estate.

By placing your policy in trust, you ensure the payout is fast, protected from Inheritance Tax, and goes directly to the people you want it to, without getting stuck in legal limbo. Most insurers offer this service for free when you take out a policy.

This simple action achieves two critical goals:

Your trustees are the people you appoint to manage the trust. Their job is to look after the payout on behalf of your children (the beneficiaries) until they are old enough to manage it themselves. It's a role of immense responsibility, so you should choose wisely.

You'll typically need to appoint at least two trustees. Good choices often include:

It’s crucial to speak with your chosen trustees beforehand to make sure they're happy to take on this role. Their duty is simply to follow the instructions you leave, ensuring the funds are used for your children’s upbringing, education, and general wellbeing. Taking this final step transforms your policy from a simple financial product into a precise and effective tool for protecting your family’s future.

As you get closer to sorting out a policy, it’s completely natural for a few final, practical questions to pop into your head. Getting clear answers to these is the last step to feeling confident you’re doing the right thing for your family.

So, let's tackle some of the most common things we get asked by parents.

Absolutely, and it’s one of the most important things for a family to consider. One of the biggest mistakes couples make is thinking that only the main breadwinner needs life insurance for parents. This completely overlooks the huge economic value a stay-at-home parent brings to the household every single day.

Just stop and think about the cost of replacing everything they do:

The bill to hire people to cover all those roles would be enormous, putting a massive financial strain on the surviving parent. A life insurance policy for a stay-at-home parent provides the cash to pay for these essential services, keeping life as stable as possible for the children during an incredibly tough time.

Insurers know that life can get in the way, and a missed payment doesn't automatically mean your cover is gone. UK providers are required to give you a grace period, which is typically 30 days from the date your payment was due.

If you pay the missed premium within this window, your cover simply carries on without a hitch. If you don't, however, your policy will lapse, and your family will no longer be protected. If you're hitting a rough patch financially, the best thing to do is call your insurer—they might be able to offer a temporary fix.

It's crucial not to let your policy lapse. If you need to take out a new one later on, it will be priced based on your current age and health, which almost certainly means you'll end up paying more.

Not always. While some applications might require a nurse screening or a report from your GP—especially for very high levels of cover or if you have a complicated medical history—it’s becoming much less common. Many UK insurers can now make a decision based purely on the health and lifestyle questions you answer on the application form.

For a huge number of healthy applicants under a certain age (often up to 50), cover can be put in place without any medical exam at all. This makes the whole process faster and much more convenient, letting you get your family protected without any fuss.

This is a classic question for couples. A joint policy is one policy covering two people. It usually pays out on the first death, and then the policy ends. Two single policies are exactly what they sound like—each partner has their own separate cover.

Let's put them side-by-side:

| Feature | Joint Policy (First Death) | Two Single Policies |

|---|---|---|

| Payout | Pays out just once, when the first person passes away. | Pays out on each person’s death, meaning two potential payouts. |

| Cost | Often slightly cheaper than buying two single policies. | Can be a little more expensive, but the difference is often small. |

| Flexibility | Less flexible. Can be tricky to sort out if a couple separates. | Highly flexible. Each policy is completely independent of the other. |

While a joint policy might save you a few quid a month, two single policies offer double the potential protection and far more flexibility for the future. For that reason, most financial advisors now recommend that couples take out two separate policies instead.

Ready to secure your family's financial future? Life Cover Plans makes it easy to compare quotes and find the right protection. Click below to get your free no-obligation quote now!

Get My Free Quote >>