At its heart, the idea of life insurance is actually very simple. Think of it as a financial safety net that you put in place for the people you care about most. You pay a regular monthly amount, called a premium, to an insurance company. In return for these payments, the company promises to pay out a tax-free lump sum of cash if you were to pass away while the policy is active. It’s all about providing crucial support at the most difficult of times.

At its core, a life insurance policy is a straightforward contract between you and an insurer. The deal is simple: your regular payments guarantee that a large sum of money—known as the 'payout' or 'sum assured'—goes to your family or chosen loved ones (your beneficiaries) after your death. This isn't just some abstract financial product; it's a practical solution to very real problems. It’s designed to shield your family from the financial fallout of losing your income. The payout can be a lifeline, used for all sorts of things:

Let's quickly break down the key parts of a typical policy.

Here are the fundamental components of a UK life insurance policy, helping to clarify how each part works for you.

| Component | What It Means For You |

|---|---|

| Policyholder | That’s you! The person who takes out the insurance and pays the premiums. |

| Insurer | The company providing the cover, which agrees to pay the claim. |

| Premium | The fixed monthly or annual payment you make to keep the policy active. |

| Sum Assured | The tax-free cash lump sum that gets paid out to your loved ones. |

| Beneficiary | The person or people you choose to receive the payout. |

| Term | The length of time the policy runs for (e.g. 25 years to match a mortgage). |

Understanding these terms is the first step to feeling confident about choosing the right protection for your family.

Here in the UK, the most common type of life insurance is a term policy. This means you're covered for a fixed period of time—say, 25 years to match the length of your mortgage. If you pass away within that term, the policy pays out. If you don't, the policy simply ends.

Their popularity is clear. Recent figures show that sales of these 'pure protection' policies grew from 242,418 in Q1 to 244,127 in Q2, with total premiums rising from £115 million to over £125 million. You can find more details in the FCA's report on life insurance sales data. This steady growth shows just how many families across the UK rely on these policies to protect their biggest financial commitments.

While term insurance is great for covering a specific period, some people want the certainty of knowing their policy will pay out no matter when they die. This is where a different type of cover comes in. For more on this, you might find our guide on how whole of life insurance works really helpful.

Ultimately, it’s all about finding a policy that feels right for your family’s unique situation and gives you genuine peace of mind.

When you first dip your toe into the world of life insurance, you’ll quickly see it splits into two main camps: Term Insurance and Whole of Life Insurance. Getting your head around the difference isn’t just about the fine print; it's the most critical decision you'll make, as it shapes exactly how, when, and why your family gets protected.

Think of Term Life Insurance as being a bit like renting a house. You're covered for a set period of time that you agree on upfront—the 'term'—which might be 20, 25, or 30 years. It’s designed to act as a financial safety net during the years your loved ones rely on your income the most.

If you were to pass away during that term, the policy pays out the lump sum. Simple. But if you outlive the term, the cover just stops, and so do your payments. Because it’s temporary, it’s by far the most affordable and popular type of life cover in the UK, perfectly matched to financial responsibilities that eventually come to an end.

Term life insurance is the go-to choice when you have specific, temporary needs in mind. Its straightforward nature and low cost make it a practical option for millions of families. It's usually the best fit if your main goal is to:

For most people, it's not a question of if term insurance is right, but how long that term should be. If you're looking for focused protection that won't break the bank, you can dive deeper into how term life insurance works.

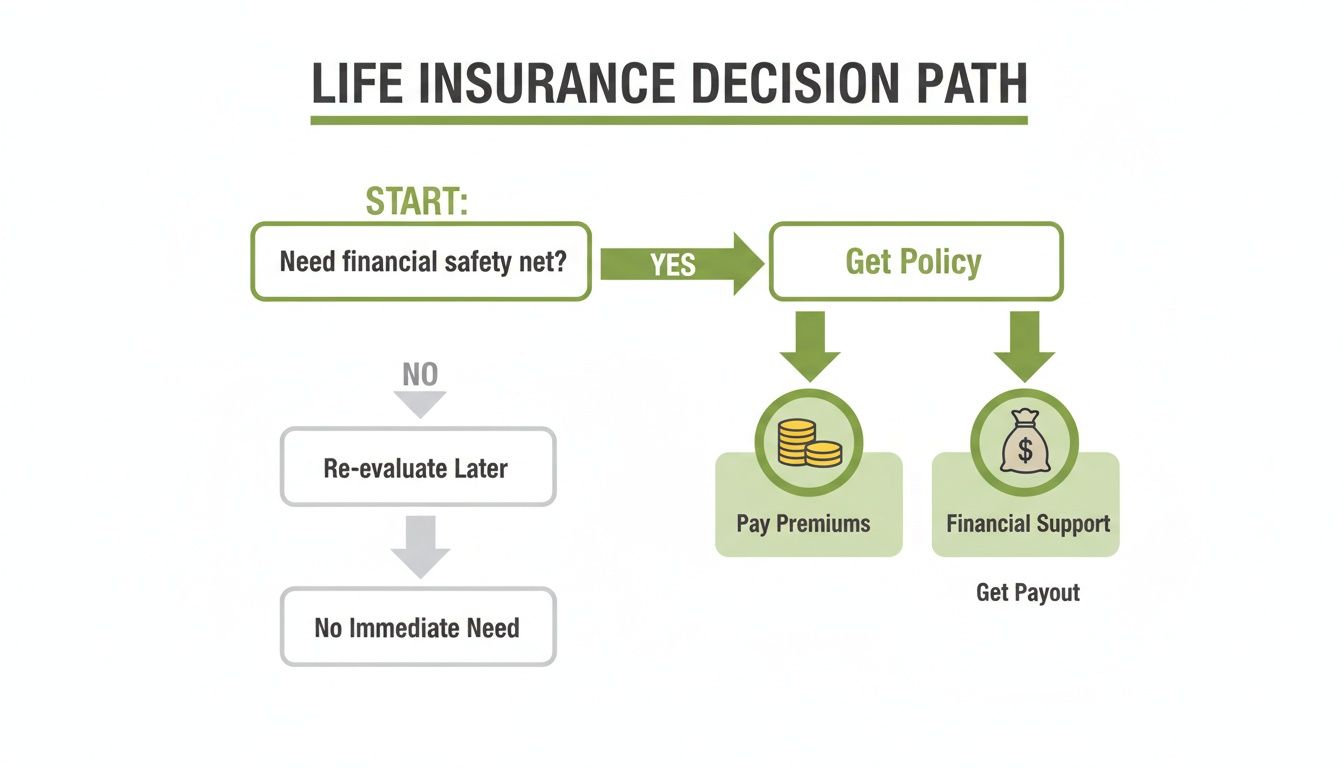

This visual shows the typical journey, from realising you need that safety net to your loved ones eventually receiving the payout.

As you can see, the whole process starts with a need. From there, your consistent premium payments are what lock in that financial security for your beneficiaries.

On the other side of the coin, you have Whole of Life Insurance. This is more like buying your home—it’s a permanent fixture. The name says it all: it covers you for your entire life. As long as you keep paying your premiums, it comes with a 100% guarantee that it will pay out when you pass away.

That guarantee makes it a completely different tool. It's less about managing debt and more about planning your legacy. People typically use it to:

This kind of permanent protection has huge appeal, especially for those over 50 who are thinking more about their estate and making sure final expenses are taken care of.

And you can have peace of mind that the insurers can deliver. The Bank of England regularly stress-tests major UK firms, which were found to hold a surplus of £21.9 billion above their requirements. That level of financial strength is what underpins the lifelong promise of a whole of life policy.

Ultimately, the right choice for you boils down to one simple question: what do you want to protect, and for how long?

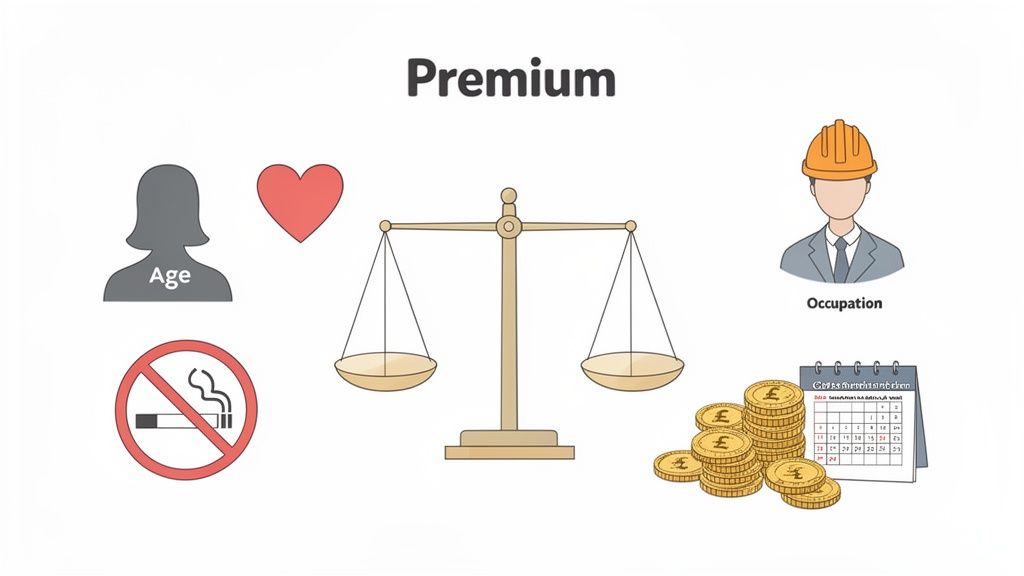

Ever looked at a life insurance quote and wondered how they actually arrived at that specific number? It’s not just plucked out of thin air. Insurers use a detailed process called underwriting, which is basically their way of building a personal risk profile just for you.

Think of it like this: the insurer is trying to work out the likelihood of a claim being made on your policy. If they see you as a lower risk, you’ll be rewarded with a lower monthly premium. It’s all about creating a price that’s fair and specific to your situation.

So, what are the ingredients that go into this calculation? While every UK insurer has its own slightly different recipe, they all look at the same core factors. Getting to grips with these helps you understand exactly what’s driving the cost.

Here are the main things that will influence your premium:

"A Quick Word on Honesty: It can be tempting to bend the truth a little—maybe not mention you smoke or downplay a health issue—to try and get a cheaper quote. Please don't. This is called 'non-disclosure', and it can give the insurer grounds to completely void your policy, leaving your loved ones with nothing when they need it most."

Beyond your personal circumstances, the two biggest levers on price are the details of the policy itself: how much cover you want, and for how long.

First, you have the Sum Assured. This is simply the lump sum that gets paid out. It stands to reason that a policy designed to pay out £500,000 will cost more each month than one for £100,000, because the insurer is taking on a much bigger financial risk.

Then there’s the Policy Term, which is how long your cover lasts. A policy running for 30 years will have higher premiums than one that only runs for 15 years, as there’s a much longer window in which a claim could happen.

Let’s put it all together. A healthy, non-smoking 30-year-old taking out £200,000 of cover over 25 years is going to pay a lot less than a 50-year-old smoker wanting the very same cover. It’s this unique combination of personal details and policy choices that creates your final price.

This is precisely why shopping around is non-negotiable. When you compare quotes, you get to see how different UK insurers weigh all these factors, allowing you to find the best possible price for your specific needs.

A standard life insurance policy is a fantastic safety net, but it’s designed to help your family after you’re no longer around. What happens if you face a serious health crisis but survive? This is where an incredibly useful add-on called Critical Illness Cover comes into play, creating a financial buffer for you while you’re still living.

Think of it as a ‘living benefit’. It’s an optional extra you can bolt onto many life insurance policies, designed to pay out a tax-free lump sum if you’re diagnosed with a specific, life-altering medical condition.

When you add critical illness cover, it sits alongside your main life insurance. If you’re diagnosed with one of the serious conditions listed in your policy documents—like certain types of cancer, a heart attack, or a stroke—the policy pays out. This happens while you’re alive, delivering immediate financial support when you and your family need it most.

It's worth knowing that this payout can affect your main life insurance. Depending on the provider, a successful critical illness claim might end the entire policy or simply reduce the final life insurance payout. Always check the small print.

The money provides a vital financial cushion, giving you the freedom to focus completely on your recovery without the stress of mounting bills. You can use the funds for anything, such as:

The list of conditions varies from one UK insurer to another, but almost all policies cover what are often called the 'big three', which make up the vast majority of claims: specific types of cancer, heart attacks, and strokes. More comprehensive policies can cover dozens of other conditions, too.

"A crucial point to grasp is that insurers have very precise definitions for each illness. For a claim to be paid, your diagnosis must meet their specific criteria. For example, a cancer diagnosis might need to be of a certain severity to qualify."

Getting to grips with these definitions is key to picking the right cover. For a deeper dive, our guide on how critical illness cover works offers more valuable detail.

Beyond critical illness, insurers offer other ways to make your policy more robust. One of the most common and valuable is the Waiver of Premium.

This nifty add-on means that if you're signed off work long-term due to illness or injury (usually after a waiting period of a few months), the insurer steps in and pays your monthly premiums for you. It ensures your life insurance and critical illness cover stay active even when your income stops. It’s a small addition that protects you from having to choose between your health and your financial security.

Taking the first step towards getting life insurance can feel like a big one, but it really doesn't need to be overwhelming. With a bit of a roadmap, you can find the right policy for your family without all the guesswork. The journey doesn't start with looking at prices; it starts by taking a clear look at your own life and what you need to protect.

This guide is all about giving you the confidence to move forward. By breaking down the process, you can make sure the protection you choose is the perfect fit for your family's future.

Before you even think about getting quotes, the most important job is to figure out the right amount of cover. This isn't a random number you pluck from the air; it's a careful calculation based on your family's actual financial picture.

Start by adding up the major financial commitments your loved ones would have to handle without you:

Once you've got a rough figure, you have a solid starting point. This simple exercise helps ensure you're not under-insured (leaving your family with a shortfall) or over-insured (and paying for cover you just don't need).

Once you know the amount of cover you're aiming for, it’s time to find the best value. My one piece of advice here is simple: never, ever take the first quote you see.

Prices can vary wildly between different UK insurers, even for the exact same level of cover. Why? Because each one has its own way of assessing risk. One might see your health or lifestyle as a higher risk than another, leading to a much higher premium.

Comparing quotes is easily the most effective way to save money on your premiums. This is where using a comparison service really comes into its own. Instead of spending hours filling out the same details on multiple websites, you can see options from a whole range of trusted providers like Aviva, Legal & General, and Royal London all in one go.

"A comparison service demystifies the whole process. It gives you an instant snapshot of the market, making sure you find a policy that's not just suitable, but also competitively priced. This simple step could save you hundreds of pounds over the life of the policy."

We’ve made our process straightforward and quick. You fill out one short, secure form, and that’s it. An FCA-authorised specialist will then give you a call to quickly run through your details, fine-tune your needs, and answer any questions you might have.

From there, you’ll get tailored, no-obligation quotes designed just for you. It's the simplest way to get to grips with how life insurance works in the UK and secure the right protection for the people who matter most.

The real worth of a life insurance policy only becomes clear during the toughest of times. Knowing how the claims process works ahead of time can lift a huge weight, giving you the confidence that the safety net you’ve put in place will actually be there for your family when they need it most.

It’s a far more straightforward process than most people imagine. It isn’t some complicated or combative system; it’s a well-established path designed to get the money to your loved ones as smoothly as possible. While the exact steps might differ slightly from one insurer to the next, the core journey is pretty much the same across the UK.

When the time comes, your family will usually just need to take a few simple actions to get the ball rolling. It all starts with a phone call or by filling out a form on the insurer's website.

From that point on, the insurer will guide them through what’s needed next. This typically involves sending over a few key documents:

Once these documents are in hand and checked, the insurer processes the claim and pays out the tax-free lump sum.

One of the most persistent myths about life insurance is that providers will find any loophole they can to avoid paying. The truth is actually the complete opposite.

The UK insurance industry pays out an incredibly high number of claims. Year after year, figures from the Association of British Insurers (ABI) show that well over 98% of all life insurance claims are successful.

"The tiny fraction of claims that are rejected almost always come down to one single issue: non-disclosure. This is just a formal way of saying the person wasn't entirely truthful about their health or lifestyle on their original application."

This really drives home the golden rule: be completely honest when you apply. As long as you give accurate information from the start, you can rest easy knowing your policy will do its job. A little bit of housekeeping, like keeping your documents in a safe, known place and simply telling your beneficiaries the policy exists, will make the process as seamless as it can be.

Even after getting to grips with the basics, it’s natural to have a few lingering questions. Let's run through some of the most common ones we hear, giving you the clear and straightforward answers you need.

Absolutely. In fact, it's quite common and often a smart move to have more than one life insurance policy. Think of it as having different tools for different jobs.

For example, you might have a big decreasing term policy that’s specifically tied to your mortgage, ensuring your family home is safe no matter what. At the same time, you could have a smaller, separate policy—perhaps a level term or whole-of-life plan—to cover funeral costs or simply to leave a guaranteed gift for your children. Stacking policies like this lets you dedicate funds for different needs.

It's a fair question. While life insurance is often seen as a safety net for dependents, it can still be incredibly useful if you're single.

Consider any debts you might leave behind, like a car loan or even a personal loan. A small policy could ensure that financial burden doesn't fall on your parents or other family members. It can also cover your funeral, which can be a surprisingly high, unexpected cost. For those who own a business, a policy could also be set up to protect a business partner from financial turmoil.

This one is really important. If you stop paying your monthly premiums, your life insurance policy will lapse. In simple terms, your cover stops.

"Once a policy has lapsed, you are no longer insured. If you passed away, your loved ones would not receive any payout. It’s absolutely vital to keep up with your payments to ensure your protection stays in place."

If you find yourself struggling to afford the premiums, your first port of call should be your insurer or broker. They may have options to help you before you’re forced to let the cover go.

For the most part, yes. In the UK, the lump sum paid out from a life insurance policy is almost always free from both income tax and capital gains tax. The potential catch, however, is Inheritance Tax.

The payout value is typically added to your estate when you die. If the total value of your estate (including the life insurance money) tips over the current £325,000 threshold, anything above that could be hit with a 40% Inheritance Tax bill.

The good news is there's a straightforward way to avoid this: write your policy 'in trust'. This simple legal arrangement keeps the policy separate from your estate, meaning the entire payout goes directly to your chosen beneficiaries, completely tax-free.

Ready to find the right protection for your family's future? The team at Life Cover Plans makes it easy to compare quotes from leading UK insurers, helping you secure the best cover at a competitive price.

Get My Free Quote >>