Critical illness cover is a specific type of insurance policy. It pays you a one-off, tax-free lump sum if you’re diagnosed with a serious medical condition that’s listed in your policy documents.

Think of it as a financial safety net, designed to catch you and your family if your health takes an unexpected turn. It’s there to protect your finances during a crisis, giving you the breathing room to focus on getting better.

Imagine a locked emergency fund that you can only access when you need it most—right after a life-altering diagnosis. That's the essence of critical illness cover. It’s not there to pay for your medical bills; that’s what the NHS and private medical insurance are for. Instead, its purpose is to help you handle the financial fallout of becoming seriously ill.

This is a crucial point. People sometimes mix it up with income protection, but they’re very different. Income protection pays you a regular monthly sum if you can’t work due to any illness or injury. Critical illness cover, on the other hand, pays out a single, large amount as soon as you're diagnosed with one of the specific conditions covered by your policy. That lump sum gives you immediate flexibility to deal with the major financial challenges that can pop up out of nowhere.

Once the money is paid out, it's entirely yours to use as you see fit. There are no strings attached, which gives you complete control during what is often a very stressful and emotional time. This financial freedom is one of the most valuable aspects of having a policy.

People use the payout for all sorts of things, such as:

The whole point of critical illness cover is to remove money worries from the equation. It allows you to concentrate fully on your recovery, without the added stress of bills piling up or the mortgage going unpaid.

When you grasp this, it's easy to see why so many homeowners and families in the UK consider it an essential part of their financial planning. It’s a shield for your finances, protecting your home and lifestyle from the devastating ripple effect a serious illness can cause. By providing that buffer, the cover helps ensure a health crisis doesn't turn into a financial catastrophe as well.

So, how does this type of cover work in the real world? It's actually more straightforward than it sounds. At its core, a critical illness policy is a deal between you and an insurance company. You pay a set amount each month (your premium), and they promise to pay you a tax-free lump sum if you're diagnosed with one of the specific illnesses listed in your policy. Simple as that.

It’s a very different beast from other types of insurance. Think of it this way: income protection replaces your monthly salary if you can't work, and private medical insurance pays for treatment. Critical illness cover gives you a one-off cash injection to use however you see fit – whether that’s clearing your mortgage, adapting your home, or just giving you breathing space to recover without financial stress.

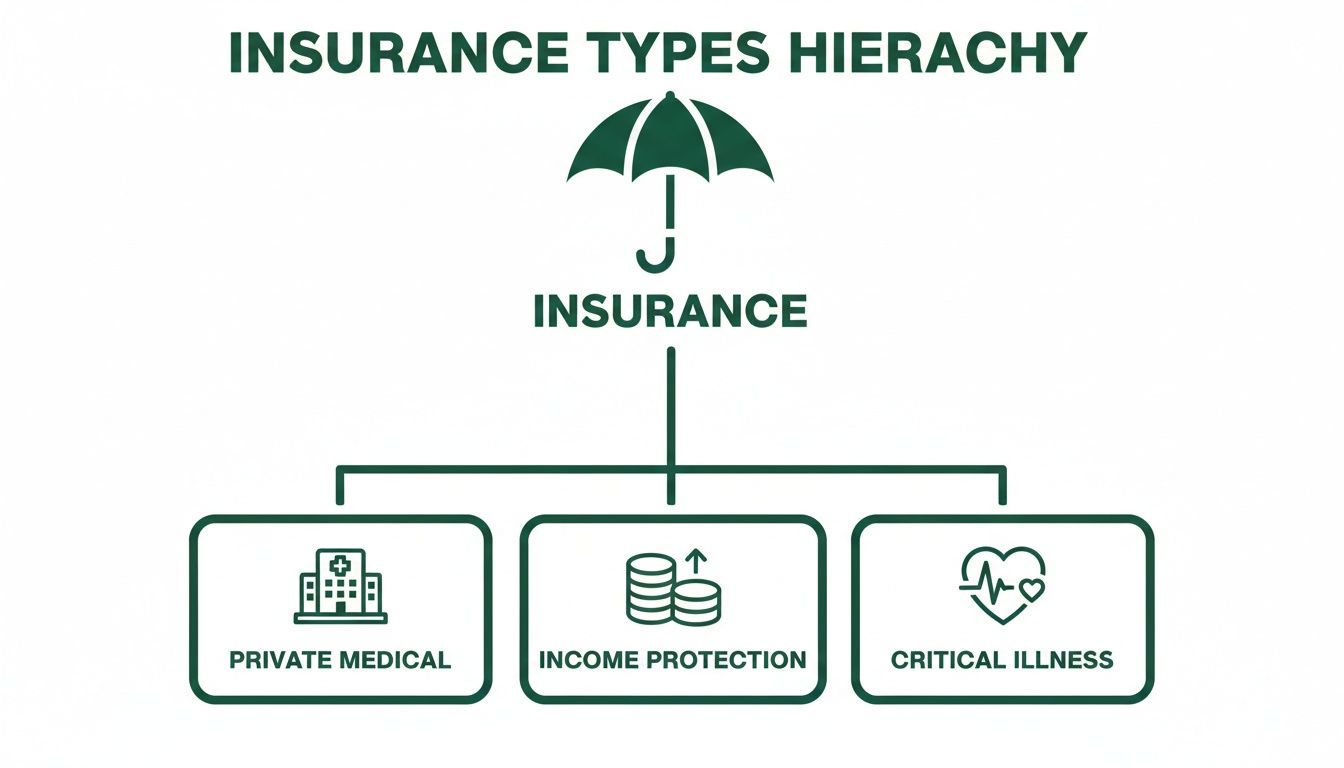

This diagram shows where critical illness cover sits among the main types of personal protection you might consider.

As you can see, each one has a distinct job to do. The unique role of critical illness cover is to provide that immediate, flexible financial lump sum right when you need it most.

When you look at getting cover, you'll come across two main ways to set it up. Each has its pros and cons, and the right one for you depends entirely on your situation.

But there’s a massive catch with combined policies that you absolutely need to know. They typically pay out only once. It's a "first claim" basis. So, if you make a claim for a critical illness, you get your payout, but then the entire policy – including the life cover part – usually ends. The policy has done its job. It’s a crucial detail that often gets overlooked.

Traditionally, critical illness cover was a bit of an all-or-nothing affair. If you were diagnosed with a specified condition and it met the insurer’s definition, you received 100% of your cover. If not, you got nothing. Thankfully, things have moved on.

Many modern policies now offer something called severity-based payouts. This is a much smarter approach that recognises not all illnesses have the same devastating impact from day one.

With a severity-based policy, you might get a smaller percentage of your total cover for a less advanced condition. For instance, an early-stage cancer diagnosis could trigger a 25% payout, leaving the other 75% of your cover in place in case things worsen or you're diagnosed with something else down the line.

This tiered system gives you a more flexible financial cushion. It provides real help for serious conditions that might not stop you from working forever, while keeping the bulk of your protection in reserve. To see what’s out there, you can compare a range of critical illness quotes and policies in the UK.

Deciding between standalone and combined cover, and getting your head around features like severity-based payouts, are the key steps. It's all about making sure the financial safety net you're building is the right fit for you and your family.

When you take out critical illness cover, it’s not a safety net for every possible health scare. Think of it more like a highly specialised insurance policy that protects you against a specific list of serious, life-altering conditions defined by the insurer.

Getting your head around this is the key to knowing what you're actually buying. The policy documents are very precise. For a claim to be successful, your diagnosis has to tick every box of the insurer’s definition. This means that simply being told you have a condition isn’t always enough – it often has to be of a certain severity to trigger the payout.

While policies can vary a lot, almost all of them are built on a foundation of the 'big three' illnesses. These are the most common reasons for claims in the UK and form the bedrock of any decent critical illness plan.

The big three are:

These three conditions consistently make up the lion's share of all claims. Cancer is by far the biggest one. For example, Royal London's 2024 data showed they paid out over £180 million for critical illness, with cancer alone accounting for a staggering 64% of claims. You can discover more insights about UK critical illness claims and see how cancer is the most common cause, especially for women, where it represents over 80% of claims.

Beyond the big three, a comprehensive policy will cover a much wider range of conditions—the number can jump from around 40 to well over 100 depending on the provider. This is a crucial area where policies really differ, and a longer, more detailed list can offer you far more robust protection.

Other conditions you’ll often find on the list include:

It’s not just about the number of conditions covered, but the quality of the definitions. A policy covering 50 conditions with fair and clear definitions is often far better than one covering 100 with strict, restrictive criteria that make it incredibly difficult to claim.

This is exactly why you need to read the small print or, even better, get some expert advice. A good adviser can help you cut through the jargon and compare the definitions from different insurers, helping you find a policy that provides genuine, meaningful protection.

It’s just as important to know what isn't covered as what is. Every policy comes with a list of exclusions—these are the specific situations or conditions that won't lead to a payout. Knowing these upfront can save a lot of heartache and confusion down the line.

These exclusions aren't there to trip you up. They exist to keep the policy affordable and focused on its real purpose: providing a financial cushion against unexpected, severe illnesses.

To give you a clearer picture, here’s a look at what’s generally covered versus what’s often left out.

| Typically Covered | Often Excluded |

|---|---|

| Invasive cancers that meet a specific severity level. | Non-invasive cancers or those treated with minor surgery. |

| Heart attacks that result in permanent muscle damage. | Angina or other heart problems that don't cause heart muscle death. |

| Strokes that cause lasting neurological symptoms. | Transient Ischaemic Attacks (TIAs), often called 'mini-strokes'. |

| Major organ failure that requires a transplant. | Health issues directly related to alcohol or drug abuse. |

| Conditions diagnosed after the policy has started. | Pre-existing conditions you already had before taking out cover. |

| Specific accidental injuries that meet the policy criteria. | Any injuries that are self-inflicted. |

Pre-existing conditions are a frequent source of confusion. If you have a medical condition before you apply, the insurer will likely do one of two things: either exclude that specific condition from your cover or charge you a higher premium. This is why total honesty on your application form is non-negotiable. Failing to disclose a health issue could give the insurer grounds to void your entire policy when you need it most.

Let's be honest, a critical illness diagnosis isn't just a health problem. It's a financial earthquake that can shake your family's world to its foundations. Suddenly, your ability to bring in a wage is up in the air, while brand-new, unexpected costs start piling up. This is the moment critical illness cover stops being just another policy and becomes a real, tangible lifeline.

The idea is simple: it’s designed to give you a single, tax-free cash payout right when you need it the most. This isn't money tied up in red tape for specific medical bills; it's a lump sum for you to use however you see fit. It gives you back a sense of control and helps reduce the financial strain during what is already an incredibly tough time.

For most of us in the UK, the mortgage is the biggest bill we face each month. The thought of falling behind on payments while battling a serious illness is a genuine nightmare. This is probably the number one reason people arrange critical illness cover.

A payout could be used to wipe out your entire mortgage balance in one go. Just imagine the sheer relief of knowing your home is safe, no matter what happens with your job. It’s a colossal weight off your shoulders, guaranteeing your family has a stable roof over their heads without the threat of repossession. For a deeper look at this, have a read of our guide on how life insurance can be used for mortgage protection.

By getting rid of that massive debt, you immediately create financial breathing space. The money that would have been swallowed by your mortgage can now go towards other essential living costs, helping you focus on getting better without worrying about money.

It’s not just the mortgage, is it? A serious illness brings a whole cascade of other expenses you might not have anticipated. The lump sum from a critical illness policy gives you the flexibility to handle these practical financial challenges.

Here are a few ways the payout can provide vital support:

The real purpose of the payout is to give you choices and control. It ensures that a health crisis doesn't force you into draining your family’s savings or making impossible financial decisions.

While anyone could benefit from this kind of safety net, it’s especially vital for people who might not have a huge financial cushion to fall back on.

It's a common myth that serious illnesses only happen to older people. Worrying new data shows that 22% of all critical illness claims in the UK are now made by people under 40. A serious diagnosis can lead to a £1 million lifetime financial hit from lost earnings and care costs, which really hammers home the importance of this cover.

This cover is particularly important if you are:

For these people, a sudden loss of income can be catastrophic. Critical illness cover acts as a cornerstone of a solid financial plan, giving you the peace of mind that your loved ones will be taken care of, no matter what life decides to throw your way.

It's one thing to know you need cover, but it’s another to feel confident about how it all works financially. Let's break down how insurers figure out your monthly payments (your premium) and what happens if you ever need to make a claim. Knowing this stuff inside out is key to peace of mind.

The price you pay isn't just a number plucked from thin air. It’s a carefully calculated risk assessment based on you as an individual. Insurers need to understand how likely it is that you might need to claim down the line.

Your monthly premium is completely personal to you. Getting to grips with what drives the cost helps you understand your quote and see where you might have some influence.

Here are the main things insurers look at:

Knowing how these levers work puts you in a stronger position. For instance, quitting smoking won't just do wonders for your health; it can also slash your insurance costs for years to come.

The idea of making a claim can feel overwhelming, especially when you're already going through a tough time. But insurers have worked hard to make the process as straightforward as possible. While the exact steps can vary a little between providers, the general journey is pretty consistent.

So, what happens if you're diagnosed with a serious illness covered by your policy?

This process isn't designed to catch you out. Insurers want to pay genuine claims, and the statistics back this up. In fact, data from early 2024 revealed that UK insurers paid out a massive £1.3 billion in critical illness claims, with the average payout being £67,600.

Choosing the right critical illness policy is a big decision, but it doesn't have to be overwhelming. If you break it down and focus on a few key areas, you can find cover that gives you and your family genuine security. The whole point is to create a financial safety net that truly fits your life.

First things first: you need to work out how much cover you actually need. A good place to start is your outstanding mortgage balance. For many people, the main goal of this insurance is to clear the mortgage, securing the family home no matter what happens.

But don't just stop at the mortgage. Think about adding a bit extra to cover your salary for a year or two while you recover. This buffer gives you vital breathing space, so you can handle everyday bills and any unexpected medical costs without draining your savings.

While the monthly premium is obviously a big factor, it’s only half the story. The real quality of a policy is hidden in the definitions. You could have two policies that look almost identical, but one might have far stricter criteria for what counts as a heart attack, making it much harder to actually make a successful claim.

It’s just as important to compare the insurer's definitions as it is to compare their prices. A policy that costs a few pounds more but has fairer, clearer definitions often represents much better value and provides real peace of mind.

This is where trying to sort it all out yourself can become tricky. The language buried in policy documents is often dense and confusing unless you know exactly what you're looking for. Trying to navigate this complex market alone can be a real headache.

Given how complex these policies can be, getting help from an independent broker is often the smartest move you can make. A specialist broker works for you, not the insurance companies. Their job is to get to know your situation—your budget, your family, your worries.

Armed with that knowledge, they can scan the whole market, comparing policies from all the leading UK insurers to find the perfect blend of price and protection for you. They’re experts at deciphering the small print and can point out the crucial differences between policies that you might easily miss. This kind of advice is invaluable. Remember, this cover is vital, but it often works best alongside other protection; you can learn more about how it complements standard term life insurance in our detailed guide.

Ultimately, getting the right protection is about making sure your family is on a stable footing during what would be an incredibly difficult time. The best way to start is by getting free, no-obligation quotes and professional advice. It’s a simple, no-pressure way to see what your options are and find a plan that delivers the peace of mind your loved ones deserve.

Even after going through all the details, it's completely normal to have a few specific questions buzzing around your head. Let's tackle some of the most common ones we hear from people thinking about critical illness cover.

This is a great question, and it gets to the heart of what this cover is really for. Sick pay from your employer is a brilliant safety net, but it's designed to handle short-term time off. Even the most generous company schemes usually only pay your full salary for a few weeks or months before it drops off or stops completely.

A serious diagnosis, on the other hand, can mean you're off work for a very long time, or you might not be able to return to your old job at all.

Think of it this way: sick pay is the first aid kit for a sprain, while critical illness cover is the major financial surgery you need for a life-changing event. The lump sum isn't just about replacing a few months' salary; it's there to clear huge obstacles like the mortgage.

The two actually work hand-in-hand. Your sick pay can tide you over initially, while the critical illness payout provides the long-term security to stop your family's finances from derailing.

Yes, you often can, but it’s not always straightforward. When you apply, the insurer will take a deep dive into your medical history – a process called underwriting. It's their way of understanding the level of risk involved.

Based on what they find, they have a few options:

Being completely open and honest on your application is crucial. If you try to hide something, you risk your insurer voiding the policy and refusing to pay out when you need it most. This is where an experienced broker really proves their worth – they know which insurers are more understanding of certain conditions and can guide you to the right place.

It’s so easy to get these two confused, but they are very different, even though they’re often sold alongside life insurance.

So, a critical illness payout is designed to help you financially through a period of treatment and recovery. A terminal illness payout is there to provide comfort and financial support during the final stage of life.

Without a doubt. It’s easy to think of this cover as just for families, but it’s arguably just as important if you’re single. If you were hit by a serious illness and couldn't work, who would pay your mortgage or rent? Who would cover the bills?

Without a partner’s income to rely on, your financial independence could vanish in an instant. A critical illness payout could be the difference between focusing on your health and facing financial ruin. It’s there to protect your home, your lifestyle, and your future.

Finding the right protection starts with understanding your options. At Life Cover Plans, we make it easy to compare quotes from the UK's leading insurers, helping you secure the peace of mind you and your family deserve. Click below to get your free no-obligation quote!

Get My Free Quote >>