When you take out a big loan, like a mortgage for your home, you want to make sure your family won’t be stuck with the debt if something happens to you. That’s exactly where decreasing term life insurance comes in.

This type of policy is often called mortgage life insurance for a very good reason. The amount of cover it provides is designed to fall over time, closely tracking the outstanding balance on a repayment mortgage.

The goal is simple: if you were to pass away during the policy term, the payout should be enough to clear the remaining mortgage, lifting a huge financial weight from your family's shoulders.

To get a quick overview, here’s a breakdown of the key features and how they work in practice.

| Key Feature | How It Works |

|---|---|

| Cover Amount | The potential payout reduces each year. |

| Primary Use | To cover a large repayment loan, like a mortgage. |

| Premiums | Typically remain fixed throughout the policy term. |

| Cost | Generally cheaper than level term insurance. |

| Purpose | Purely protection, with no investment or cash-in value. |

This table shows how the policy is built specifically to handle a debt that gets smaller over time, making it a very efficient form of protection.

Let's imagine you've just bought your first home with a £250,000 mortgage over 25 years. You'd take out a decreasing term policy with a starting cover amount of £250,000 and a term of 25 years.

In the early years, when your mortgage balance is high, your life cover is at its maximum. Fast forward 15 years, and you’ve paid off a good chunk of the loan. By this point, your insurance cover will have also dropped to roughly match the smaller, remaining mortgage balance.

Think of it as a safety net that's perfectly sized for the debt at any given time. It’s not designed to leave a lump sum for other expenses; its one and only job is to make sure your home is secure.

The single-minded focus on protection, rather than investment, is what makes this policy so cost-effective.

Because the insurer's potential payout gets smaller every year, their risk decreases, too. This lower risk is passed on to you in the form of cheaper monthly premiums compared to a level term policy, where the payout amount stays the same from start to finish.

In fact, research from Reassured, a major UK broker, found that the average cost for this type of cover was just £29.75 per month. This affordability makes it a popular choice for homeowners looking for straightforward peace of mind.

A decreasing term policy isn’t about leaving a financial windfall. It’s about eliminating a specific financial liability, ensuring your family isn't left with a mortgage to pay.

This is what makes it such a good fit for anyone with a repayment mortgage. If you want to dive deeper into how this works for home loans, take a look at our complete guide on mortgage life insurance. By getting quotes from trusted UK insurers, you can find a plan that protects your home without stretching your budget.

To really get your head around decreasing term life insurance, it helps to picture how it lines up with your mortgage. Imagine a graph tracking your mortgage over, say, 25 years. One line shows your outstanding loan balance, starting high and steadily dropping towards zero with every monthly payment.

Now, imagine a second line running just above it, representing your life insurance payout. This line also slopes downwards, mirroring your mortgage balance. The whole point is to ensure that if the worst happened, the payout would be just enough to clear the remaining debt at any given time.

This direct link to a repayment mortgage is what makes this type of cover so specific and cost-effective. It's designed for one primary job: protecting your home.

This is where people often get a bit confused. If the amount of cover is dropping each year, surely the monthly premium should drop too, right? Surprisingly, no.

One of the best things about this policy is that your monthly payments are fixed for the entire term. The price you agree on day one is the same price you’ll be paying in the final year. Insurers work out a level premium by averaging out the risk over the whole policy, which gives you a predictable cost you can easily budget for.

The trade-off is simple. You accept that the potential payout will reduce over time, and in return, you get a much cheaper premium than you would with level term insurance, where the payout stays the same.

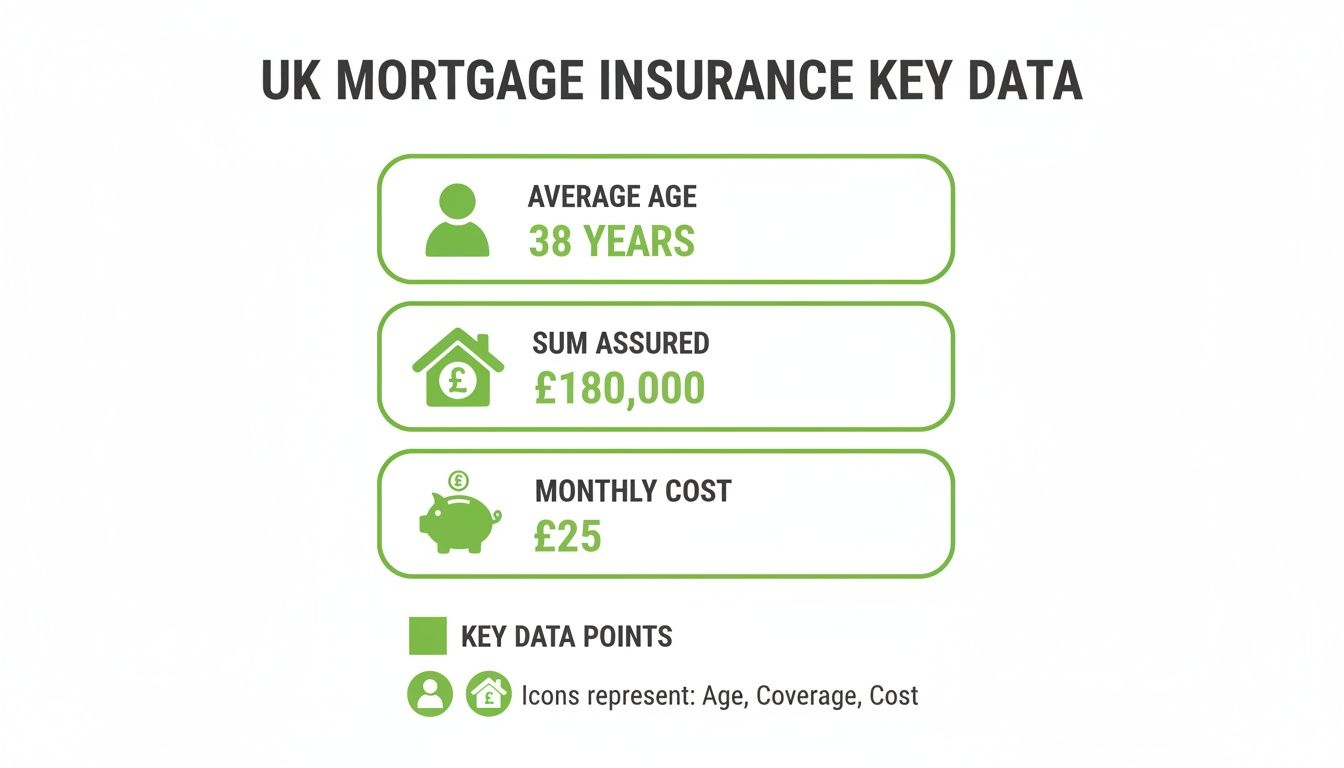

The infographic below gives you a snapshot of some typical figures for this kind of mortgage protection in the UK.

As you can see, it’s a way to secure a large amount of initial cover for a relatively low monthly cost, which is why it's such a popular choice for homeowners.

This kind of focused cover is vital in the UK, where many families are underinsured and financially exposed. Shockingly, UK households with dependents have an average life insurance shortfall of £89,800. For those with children, that figure leaps to an eye-watering £194,200.

Decreasing term policies are a direct solution to this problem for homeowners, as they are designed to cover the single biggest debt most people will ever have: their mortgage. You can read more about these figures and the scale of the UK's insurance shortfall.

The core principle is simple: Your cover reduces because your need for it reduces. The policy provides what’s necessary to clear the debt, nothing more and nothing less, which is the key to its affordability.

By perfectly matching the payout to the loan, it stops you from paying for more cover than you need in the later years. It’s a lean, efficient way to protect your home, making it a cornerstone of financial planning for anyone with a repayment mortgage.

When you're looking at life insurance, it can feel like you've arrived at a fork in the road. You'll often find two main paths ahead: decreasing term and level term insurance. They both offer your family vital protection, but they get there in very different ways. The key to choosing the right one is to first ask yourself a simple question: what exactly am I trying to protect?

Your answer will almost always point you in the right direction. If your main goal is to cover a specific debt that gets smaller over time—like a standard repayment mortgage—then one policy is a natural fit. But if you want to leave behind a fixed cash lump sum for your loved ones, no matter what, then the other is the clear winner.

Getting this right is crucial. It means your family gets the exact cover they need, and you aren't paying for more than you have to.

The biggest distinction between these two policies comes down to the sum assured – that's the amount of money that gets paid out if you pass away during the policy's term.

This one fundamental difference shapes everything else, from what each policy is best used for to how much you’ll pay for it each month.

Let's walk through a couple of real-world examples to see how this plays out.

Scenario A: The Mortgage Protector - Imagine you’ve just taken out a £250,000 repayment mortgage on your new family home, set over a 30-year term. Your number one worry is making sure that if something happened to you, your partner wouldn't have to sell the house to pay off the remaining debt.

In this case, decreasing term life insurance is the perfect tool for the job. You can set up a policy to start at £250,000 and run for 30 years. As you steadily pay off your mortgage, the insurance cover will drop in line with it, ensuring there's always just enough to clear the outstanding balance.

Scenario B: The Family Legacy - Now, let's picture a different situation. Your mortgage is all paid off, but you want to leave a financial safety net for your kids. You want to make sure they have £150,000 to help with university, a deposit for their own home, or just a solid start in life, regardless of when you might pass away.

Here, level term insurance is the way to go. A decreasing policy just wouldn't work because the payout shrinks over time. A level term policy, on the other hand, guarantees that the full £150,000 will be there for them, providing the certainty you're looking for.

Because the insurer's potential payout gets smaller year after year with a decreasing term policy, the risk for them also reduces. This is reflected in the price. Premiums for decreasing term cover are almost always cheaper than for a level term policy with the same starting sum assured.

For both policy types, your premiums are usually fixed. This means the amount you pay each month won't change, which makes it easy to budget for. If finding the most affordable protection is a priority, it’s worth exploring the different types of term life insurance available to find the right balance of cost and cover.

To really make the differences clear, let's lay them out side-by-side. This table gives you a quick snapshot to help you decide which policy aligns best with your needs.

| Feature | Decreasing Term Insurance | Level Term Insurance |

|---|---|---|

| Payout Amount | Reduces over the policy term. | Stays the same throughout the policy term. |

| Primary Purpose | To cover a repayment loan, like a mortgage. | To provide a fixed lump sum for family protection or inheritance. |

| Monthly Premiums | Lower, as the insurer's risk decreases. | Higher, as the payout amount is fixed. |

| Best For | Homeowners with a repayment mortgage. | Families needing a financial safety net or inheritance planning. |

| Value Over Time | The protection value is designed to match a shrinking debt. | The real-term value can be eroded by inflation over time. |

In the end, the "best" policy is simply the one that solves your specific financial challenge. By understanding how decreasing term cover works and where it differs from its level term counterpart, you can make a confident choice to protect what matters most to you.

So, is decreasing term life insurance the right choice for you? The answer really hinges on one simple question: what specific debt are you trying to protect? This isn't a catch-all policy; it’s more of a specialist tool, designed for a very specific job. For some people, it’s hands down the most efficient and affordable protection you can get.

Its real strength is how neatly it mirrors large repayment loans. If your biggest worry is leaving your loved ones saddled with a hefty mortgage, this type of cover should be high on your list. It's designed to give you peace of mind that, no matter what happens, your family can stay in their home.

Let's think about a real-world example. Picture James and Sarah, a couple in their early 30s. They've just taken the plunge and bought their first home with a 30-year repayment mortgage. With a baby on the way, their number one concern is making sure the house is secure. They don't have a massive savings pot, so they need pure protection at the lowest possible cost.

This is where a decreasing term policy fits perfectly. The cover starts high, matching their mortgage from day one, and then gradually reduces as they pay it off. This clever structure means they are never paying for more cover than they need, and their premiums are much lower than they would be for a level term policy. That frees up cash for everything else that comes with a growing family.

This scenario gets to the heart of what is decreasing term life insurance: it provides just enough money to clear the mortgage—nothing more, nothing less.

The prime candidates for this policy are individuals or couples whose biggest financial headache is a repayment loan. It offers precise, cost-effective peace of mind that shrinks in line with their debt.

With household budgets getting tighter across the UK, affordability is a big deal. Recent analysis projects that premium growth for life insurance is likely to slow down due to pressure on people's incomes, making cost-effective options like this more popular than ever. With an average monthly cost of just £29.75, it's one of the cheapest ways to protect a mortgage, which is crucial when you learn that only 28% of UK adults have any life insurance at all. You can read more about these UK life insurance trends and projections.

While it's a fantastic solution for many, it’s not for everyone. Knowing who this policy isn't for is just as important as knowing who it's for. The main drawback is baked right into its design: the payout gets smaller over time.

Here are a few situations where another type of policy would probably make more sense:

Ultimately, choosing this type of insurance is a strategic move. It’s for people who’ve looked at their finances, identified the mortgage as the biggest single risk, and want a lean, affordable way to cover it. By matching your protection directly to your debt, you ensure your family’s home is safe without paying a penny for cover you simply don't need.

Every financial product has its good and bad points, and decreasing term life insurance is no different. It’s a very specific tool built for a very specific job. For some people, it's the perfect solution, but it’s definitely not a one-size-fits-all policy.

To figure out if it's the right fit for you, you need to look at both sides of the coin. The big draw for most UK homeowners is the price tag – it's incredibly affordable. But that low cost comes with a few trade-offs you absolutely need to be aware of.

The real beauty of this policy lies in its simplicity and efficiency. It’s designed to do one thing exceptionally well: protect a repayment loan without any expensive frills.

Here's where it really shines:

At its heart, this policy is all about efficiency. It gives you a safety net that’s sized just right for your biggest debt, making sure your family can keep their home without you paying a penny more than you have to.

While it’s a brilliant tool for mortgage protection, the very things that make it so affordable are also its biggest limitations. It's vital you understand these drawbacks before you sign on the dotted line.

Here are the main things to watch out for:

So, you're ready to get your mortgage protection sorted? Fantastic. Finding the right decreasing term policy is actually pretty straightforward once you know what you’re doing. It all boils down to a few key decisions that will make sure the cover you get is a perfect fit for your mortgage and your family.

First things first, you need to get two numbers spot on: the sum assured (that’s the starting amount of cover) and the policy term. It’s simple really – the sum assured should be the same as your mortgage balance, and the term should match the number of years you have left to pay it off.

For example, if you've just taken out a £300,000 mortgage over 25 years, you’ll want a £300,000 policy that runs for a 25-year term. Getting this right is the foundation of a solid policy.

With the basics covered, you need to think about who the policy is for. Will a single policy do the job, or is a joint one better? A single policy covers one person. A joint policy covers two people, but—and this is a big but—it usually only pays out once, on the first death.

While a joint policy might seem a little cheaper upfront, taking out two separate single policies gives you twice the protection. That’s because each policy would pay out independently if the worst happened, giving your family a much bigger safety net.

Next up, you should think about adding any optional extras. One of the most common and, frankly, most valuable additions is Critical Illness Cover.

This add-on pays out a tax-free lump sum if you're diagnosed with a serious illness specified in the policy, like a heart attack, stroke, or certain cancers. It can be an absolute financial lifeline, helping you keep up with mortgage payments while you focus on getting better.

Of course, adding critical illness cover will bump up your monthly premium, but the peace of mind it offers is often well worth it. That money can be used for anything you need – adapting your home, covering lost income, or paying for private treatment. It turns a standard life policy into a much more comprehensive safety net.

For some people, mortgage protection is just one piece of the puzzle. If you're thinking about things like inheritance tax planning or leaving a guaranteed lump sum behind, you might find that a different type of cover is more suitable. You can learn more about this in our guide to whole of life insurance policies.

Ultimately, the best way to get a great deal on a policy that ticks all your boxes is to compare quotes from the big UK insurers like Aviva, Royal London, and Zurich. Using a service like ours at Life Cover Plans makes this easy, laying out all your options in one place. By following these steps, you can find the right cover to protect your home and family with total confidence.

To wrap things up, let's dive into a few common questions people ask when they're looking at decreasing term life insurance. Getting these practical points cleared up should give you the confidence you need to decide if it's the right fit for you and your family.

Yes, you can almost certainly still get cover. The most important thing is to be completely upfront about any pre-existing conditions on your application form. Don't hide anything.

Insurers look at every application individually. Based on what your condition is and how severe it is, they might:

It’s very rare to be declined outright, and since every insurer has slightly different rules, it's always worth getting a few quotes.

This is a great question. Your policy isn't linked to your house, but to the mortgage loan you took out to buy it. So, if you move and get a bigger mortgage, your old policy probably won't be enough to cover the new, larger debt.

Moving house or remortgaging is the perfect trigger to review your life insurance. You'll need to check if your cover amount and the remaining term still line up with your new loan. Often, it makes sense to take out a new policy to make sure you're not leaving your family under-protected.

Absolutely, and it's a very popular thing to do. Bolting on critical illness cover can turn a good policy into a great one.

With this added, the policy pays out if you're diagnosed with a serious illness specified in the policy terms, like a stroke, heart attack, or certain cancers. That lump sum can be a real lifeline, helping you pay the mortgage and other bills while you focus on getting better. It adds a much stronger layer of financial security.

They might both feel like a financial safety net, but they're designed for very different jobs. Decreasing term life insurance is there to pay off a specific debt—usually your mortgage—with a single lump sum if you die.

Income protection insurance, on the other hand, is all about replacing your salary. If you can't work because of an illness or injury, it pays you a regular monthly amount to cover your day-to-day living costs. It’s not designed to clear a huge debt in one go. For total peace of mind, many people actually have both.

Ready to secure that peace of mind for your family and home? At Life Cover Plans, we make it simple to compare quotes from the UK's leading insurers, helping you find the right cover at the right price. Click below to get your free quote now!

Get My Free Quote >>