It's the big question on everyone's mind: what does life insurance actually cost? The simple answer is that it’s often far more affordable than most people assume. While your final premium will always be unique to you, getting a feel for the ballpark figures is the perfect place to start.

Thinking about life insurance can feel a bit like trying to hit a moving target. With so many different factors at play, it’s easy to jump to the conclusion that protecting your family is going to be expensive.

The reality, however, is often quite different. For many people, putting a really solid financial safety net in place can cost less than a weekly coffee from your favourite cafe.

Recent data from the UK's largest broker paints a clear picture of just how accessible this cover can be. The average monthly cost for term life insurance recently dropped to just £32.64, for an average payout of over £160,000. It just goes to show how much protection you can get for a relatively small monthly payment.

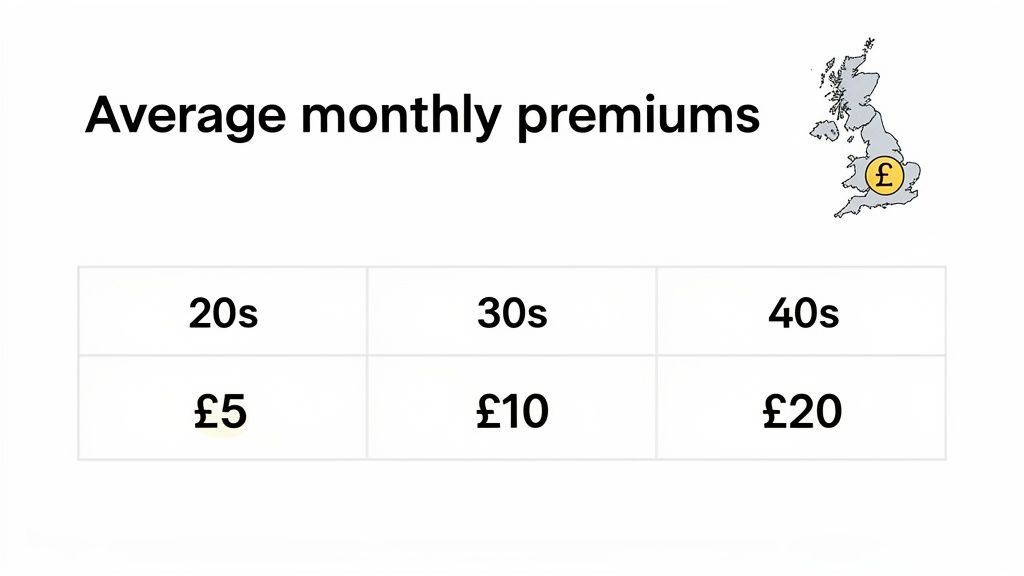

To give you a clearer idea of how this looks in practice, let's break it down by age. The table below shows some typical monthly costs for a non-smoker looking for £100,000 of level term cover over 25 years. This is a really common scenario for someone wanting to cover their mortgage or make sure their family is provided for until the kids are grown up.

The table below shows the typical monthly cost of life insurance for non-smokers at different stages of life, based on a £100,000 level term policy over 25 years.

| Age Group | Average Monthly Premium |

|---|---|

| 20s | £5 - £8 |

| 30s | £8 - £12 |

| 40s | £12 - £20 |

| 50s | £25 - £45 |

These numbers act as a fantastic guide and really drive home one of the core principles of life insurance: the younger and healthier you are when you get cover, the cheaper your premiums will be.

Key Takeaway: Your age is one of the single biggest factors in what you'll pay for life insurance. By taking out a policy earlier in life, you lock in a much lower rate for the entire term, which could save you thousands of pounds over the years.

This quick overview really sets the stage for understanding the bigger picture. Age is a crucial starting point, but it's just one piece of the puzzle. A few other key elements all work together to shape your final quote.

The main things that influence the price you’ll pay include:

By getting to grips with these core components, you can start to see how your own circumstances will affect the average cost of life insurance in the UK. In the next few sections, we’ll dive into each of these factors in much more detail.

Before we get into the numbers, it's crucial to understand what you’re actually buying. Choosing a life insurance policy is a bit like picking a car; a two-seater sports car is useless if you need to do the school run with three kids. Each policy is built for a different job, and matching the right one to your circumstances is the first step towards getting real value for your money.

Getting your head around the options means you won't pay for features you don't need or, even worse, end up with a policy that doesn't actually protect your family in the way you intended. Let's break down the main types you'll find in the UK so you can see which one is the perfect fit.

Think of term life insurance as renting your protection. You decide how long you need the cover to last (the "term") and pay a fixed monthly premium for that time. If you pass away within that period, your loved ones get a tax-free lump sum. If you outlive the term, the policy simply ends, and you stop paying.

This is by far the most popular and generally the most affordable type of life insurance. Because it only covers you for a specific window of time, the risk to the insurer is lower, which means lower monthly payments for you.

Decreasing term insurance, often called mortgage life insurance, is a specialist version of a term policy. The key difference is that the potential payout shrinks over time, usually in line with the outstanding balance of a repayment mortgage.

The logic is simple: as you pay off your mortgage, the amount of debt you need to cover gets smaller. Your policy mirrors this, making sure your family could clear whatever is left on the mortgage if you were no longer around. Because the cover amount goes down, the premiums are typically cheaper than a standard term policy.

Unlike term insurance, whole of life insurance is more like owning your protection outright. It covers you for your entire life, guaranteeing a payout to your beneficiaries whenever you pass away, as long as you’ve kept up with the payments.

Because the payout is a certainty, not a 'what if', these policies are more expensive than term insurance. They usually serve a very different purpose, moving beyond protecting against debts to focus more on legacy planning.

A whole of life policy provides a guaranteed lump sum, making it a reliable tool for covering final expenses like funeral costs, which currently average around £4,000 in the UK. It can also be used to cover a potential inheritance tax bill.

Ever wondered why the life insurance quote you get is so different from your friend's, even if you’re a similar age? It all comes down to how insurers calculate risk.

Think of it like a car insurance company sizing up a driver. They look at your driving history, the car you drive, and even your postcode to figure out the odds of a claim. Life insurers do something similar, but their focus is squarely on your health and lifestyle.

Getting your head around these factors is a game-changer. It pulls back the curtain on the pricing process and shows you exactly where you have some control over the final cost. Insurers zero in on a handful of key areas to build a personal risk profile, which translates directly into the monthly premium you'll be offered.

Let's break down the main things that go into your quote.

Your age is the big one. It’s the single most important factor, full stop. As we get older, the statistical chances of developing health problems creep up, which means the insurer's risk of having to pay out increases, too.

This is exactly why it’s almost always cheaper to get a policy sorted when you’re younger. By doing it sooner, you lock in a lower premium for the entire life of the policy.

Right alongside age, your current health plays a massive role. During the application, you'll be asked about:

This info helps the underwriter—the expert who assesses your application—to place you in a risk category. A clean bill of health will always land you a much better price.

Your day-to-day habits give insurers a glimpse into your long-term health prospects. And the most impactful choice by a mile? Smoking.

Using any tobacco or nicotine products, including vaping, automatically puts you in a higher-risk bracket.

Insurers view smokers as having a significantly shorter life expectancy, which can cause their premiums to be double or even triple that of a non-smoker for the exact same amount of cover. The financial incentive to quit is enormous.

Other lifestyle factors also come into play, like your alcohol consumption or whether you’re into high-risk hobbies like rock climbing or motorsports. Honesty is always the best policy here. Giving inaccurate information could lead to your policy being cancelled, leaving your family with nothing when they need it most.

It might not seem obvious, but your job can also affect your premium. An office worker will typically pay less than someone in a more hazardous role, like a construction worker on high scaffolding or an offshore oil rig worker. The insurer is simply factoring in the increased day-to-day risk.

Finally, the nuts and bolts of the policy you choose have a direct and clear impact on the cost:

By understanding how these five elements—age, health, lifestyle, job, and policy details—all fit together, you can go into your application with a much clearer view of how insurers see you. This knowledge puts you in the driver's seat, helping you make smart decisions to find the best-value protection for your family.

Right, let's get down to the brass tacks. We’ve covered the theory, but seeing the actual numbers is what really brings it home. It’s one thing to know that being younger or a non-smoker helps; it’s another to see the pound-and-pence difference it makes to your monthly budget.

This is where we move from concepts to concrete examples. We’ll break down some sample monthly premiums for different ages, cover amounts, and policy lengths. Most importantly, you'll see a crystal-clear comparison of costs for smokers versus non-smokers, which is easily the biggest lifestyle choice you can make to slash your premiums.

These figures will help you get a realistic feel for what you might pay, giving you a solid starting point before you begin comparing quotes.

As we’ve said, the golden rule with life insurance is simple: younger equals cheaper. To an insurer, a 25-year-old is a much lower risk than a 45-year-old, and that’s reflected directly in the price. The amount of cover you need also plays a straightforward role—the bigger the potential payout, the higher the monthly premium.

Let’s look at some typical monthly costs for a level term policy over 25 years for a healthy non-smoker.

| Age | £100,000 Cover | £250,000 Cover | £500,000 Cover |

|---|---|---|---|

| 30 | ~ £8 per month | ~ £14 per month | ~ £25 per month |

| 40 | ~ £13 per month | ~ £26 per month | ~ £48 per month |

| 50 | ~ £30 per month | ~ £68 per month | ~ £130 per month |

The trend is impossible to miss. A 30-year-old can lock in half a million pounds of cover for about £25 a month. Fast forward to age 50, and that same level of protection could cost over five times as much. This is exactly why it pays to get cover sorted earlier rather than later.

Of all the lifestyle factors, nothing sends your life insurance premiums soaring quite like smoking. Insurers see smoking or using any nicotine products (and yes, that includes vapes) as a major health risk, which translates directly into higher costs. For many providers, premiums for smokers can be double—or even more—than for non-smokers.

The difference isn't just a few quid. Over the life of a 25-year policy, a smoker could easily pay thousands of pounds more than a non-smoker for the exact same amount of cover. It's one of the most powerful financial reasons to quit.

Let's put some numbers to it. Here are sample monthly costs for a £200,000 level term policy over 25 years.

| Age | Average Monthly Premium (Non-Smoker) | Average Monthly Premium (Smoker) |

|---|---|---|

| 30 | £11.50 | £19.00 |

| 40 | £20.00 | £38.00 |

| 50 | £49.00 | £105.00 |

As you can see, the gap gets much wider as you get older. A 40-year-old smoker is paying nearly double, and by 50, the premium is more than twice as high. The good news? If you've been completely nicotine-free for at least 12 months, insurers will usually class you as a non-smoker, which can lead to massive savings.

Finally, the type of policy you choose makes a huge difference to the price. A term policy, which covers you for a fixed period, is always going to be the most affordable option. In contrast, a whole of life policy, which guarantees a payout no matter when you pass away, comes with a much higher premium.

This is simply because the payout is a certainty, not a possibility. If you want to dive deeper, you can learn more about how whole of life insurance policies are put together.

By looking at these tables and examples, you can start to build a much clearer picture of life insurance costs in the UK and see exactly how your own circumstances will shape the final price.

Knowing what drives the average cost of life insurance is one thing, but actually getting a handle on those costs is where it really counts. While you can't turn back the clock on your age, you have far more control over your monthly premium than you might think. With a few smart decisions and proactive changes, you can lock in fantastic protection for your family at a much better price.

Lowering your premium isn't about cutting corners or settling for less cover. It's about showing an insurer that you're the lowest possible risk. Let's walk through the most effective ways to slash your costs and find the absolute best value.

Your current health and day-to-day habits play a massive role in the final quote you receive. Insurers love applicants who look after themselves, so any steps you take to improve your well-being can lead to direct savings.

Paying for too much cover is a classic, expensive mistake. Choosing a policy that’s perfectly matched to your financial goals means you're not wasting money on protection you simply don't need. The perfect example is protecting your mortgage.

For a standard repayment mortgage, a decreasing term policy is almost always the most cost-effective option. The amount of cover shrinks over time, perfectly in sync with your shrinking mortgage balance. You only ever pay for the protection you actually need, making it significantly cheaper than a level term policy for the same starting amount.

It's the same story with the policy length. If your main goal is to protect your kids until they fly the nest, a 20-year term is a much better and more affordable fit than a 35-year term. Always match the policy to the problem you're trying to solve.

While looking after your health is brilliant, the single most effective action you can take to get a lower premium is to compare quotes from multiple insurers. Every single provider has its own rulebook for assessing risk.

One insurer might see a minor health issue and offer you a standard price, while another might view it differently and give you a preferred rate that's 20-30% cheaper. You'll never know who offers the best deal for your personal situation unless you shop around.

Using a comparison service like Life Cover Plans is the simplest way to do this. Instead of drowning in paperwork, one quick form gives you access to quotes from a huge panel of the UK's top insurers. This guarantees you find the most competitive price out there, turning a confusing task into a simple, money-saving win.

You've done the hard work of understanding what goes into the average cost of life insurance UK and what makes a policy tick. Now it's time for the easy bit: turning that knowledge into a real, personalised quote. This isn't about a sales pitch; it's about putting the tools in your hands so you can make a smart, confident decision for your family.

The whole process is refreshingly simple and puts you firmly in the driver's seat. It all kicks off with a quick, secure online form that takes just a minute or two to fill out.

Finding the right cover is a clear, three-step journey. There are no hidden fees or complicated hoops to jump through—just a straightforward route to getting that all-important peace of mind.

This approach takes all the legwork and guesswork out of it. Instead of spending hours contacting insurers one by one, you get a bird's-eye view of the market in one go.

Our Promise to You: This service is completely free to use. There is zero obligation to take any of the quotes you receive. We're just here to give you the information you need to choose what's right for you, in your own time.

By comparing your options, you make sure you’re not just getting any policy, but the right policy at the best possible price. Taking a few moments right now to compare free, no-obligation quotes could lock in your family’s financial future and save you a tidy sum on your monthly premiums. It's the smartest final move you can make to protect the people who matter most.

Working out the average cost of life insurance is a big step, but it usually sparks a few final questions. To wrap things up, we’ve put together clear, simple answers to the queries we hear the most from people just like you. Think of this as the last piece of the puzzle, designed to give you the confidence to move forward.

There’s no magic number here – the right amount of cover is completely personal. A common rule of thumb is to aim for a payout that’s around 10 times your annual salary, but a more accurate way is to properly crunch the numbers for your own family.

Take a look at these key areas:

Once you’ve added all that up, just subtract any savings or existing cover you already have. What's left is a really solid estimate of the cover your family would realistically need to keep their lives on track.

Yes, in most cases, you absolutely can. It’s a huge misconception that having a health condition like diabetes, high blood pressure, or a history of mental health issues is an automatic "no" from insurers. The reality is, they’re experienced in assessing a massive range of conditions every day.

While your premium might be higher than for someone with a clean bill of health, many specialist insurers can still offer competitive rates. The most important thing is to be completely honest on your application. Disclosing your full medical history makes sure your policy is valid and will actually pay out when your family needs it most.

Getting cover with a medical condition is often much more straightforward than people think. By comparing quotes from different providers, you can find an insurer who understands your specific situation and offers the most favourable terms.

Ultimately, life insurance is about buying peace of mind. It's a small, regular payment that locks in a huge financial safety net for your loved ones if the worst should happen.

For a monthly cost that is often less than what you’d spend on takeaway coffees, you can make sure your mortgage is paid off and your family’s lifestyle is protected. The true value isn't just financial; it's the reassurance of knowing you've secured their future, no matter what comes next.

Ready to see your personalised options? You can start a free, no-obligation comparison today at Life Cover Plans. Click below to get you're free quote!

Get My Free Quote >>