Life and critical illness cover is a bit like a two-in-one financial safety net. It’s a single insurance policy designed to pay out a tax-free lump sum just once, but it has two triggers: you're either diagnosed with a serious illness that’s covered, or you pass away.

It bundles these two powerful types of protection together, making sure your family gets crucial financial support when they need it most.

Picture your income as a big, sturdy umbrella protecting your family from life’s financial storms—keeping the mortgage paid, the bills covered, and future plans on track. It does a great job against the usual drizzle.

But what happens if a real tempest hits? A life-changing illness or your unexpected death are two of the fiercest storms any family can face.

Life and critical illness cover is designed to be that very umbrella, but reinforced to withstand those specific crises. It combines two essential layers of protection into one straightforward policy, providing a single source of help during an incredibly tough time.

The best way to think about a combined policy is that it’s waiting for one of two events to happen. While it only ever pays out once, it gives you and your family a much broader layer of security.

At its heart, a combined policy simply asks, "Which happens first?" If you get seriously ill, it pays out then and the policy ends. If you pass away without a prior illness claim, it pays out then. It's a single pot of money, ready and waiting for whichever of these two life-changing events comes first.

This dual-trigger structure creates a really robust financial backstop. Instead of you worrying about how your family would manage the mortgage after a sudden diagnosis or your death, you’ve already put the solution in place. It’s less of an insurance policy and more of a pre-planned strategy that shields your family from financial chaos, letting them focus on what truly matters—your recovery, or grieving without the added burden of money worries.

Getting your head around how a combined life and critical illness cover policy works is much simpler than it sounds. At its heart, the policy operates on a straightforward ‘one-and-done’ principle. This means it’s designed to pay out a single, tax-free lump sum on the first valid claim, and once that happens, the policy ends.

Whether that first claim is for a serious illness or upon death, the core function is the same. The policy doesn’t pay out twice; it’s there to provide a financial lifeline for whichever of these two life-changing events happens first. Grasping this is key to understanding why this cover is such a vital safety net for families when they need it most.

Let’s put this into practice. Imagine Sarah and Tom, a couple in their late thirties with two young children and a £250,000 mortgage on their home in Manchester. They decide to take out a joint life and critical illness policy to make sure their family and their home are protected.

A few years down the line, Tom is diagnosed with a severe heart condition that’s listed on their policy. After they submit the claim with the necessary medical evidence, their insurer pays out the full £250,000.

Once that claim is paid, their policy simply ends. If Tom had passed away without having made an illness claim first, the life insurance part of the policy would have triggered the exact same payout to Sarah, making sure she could cope financially. It’s all structured to deliver support at that first critical moment of need.

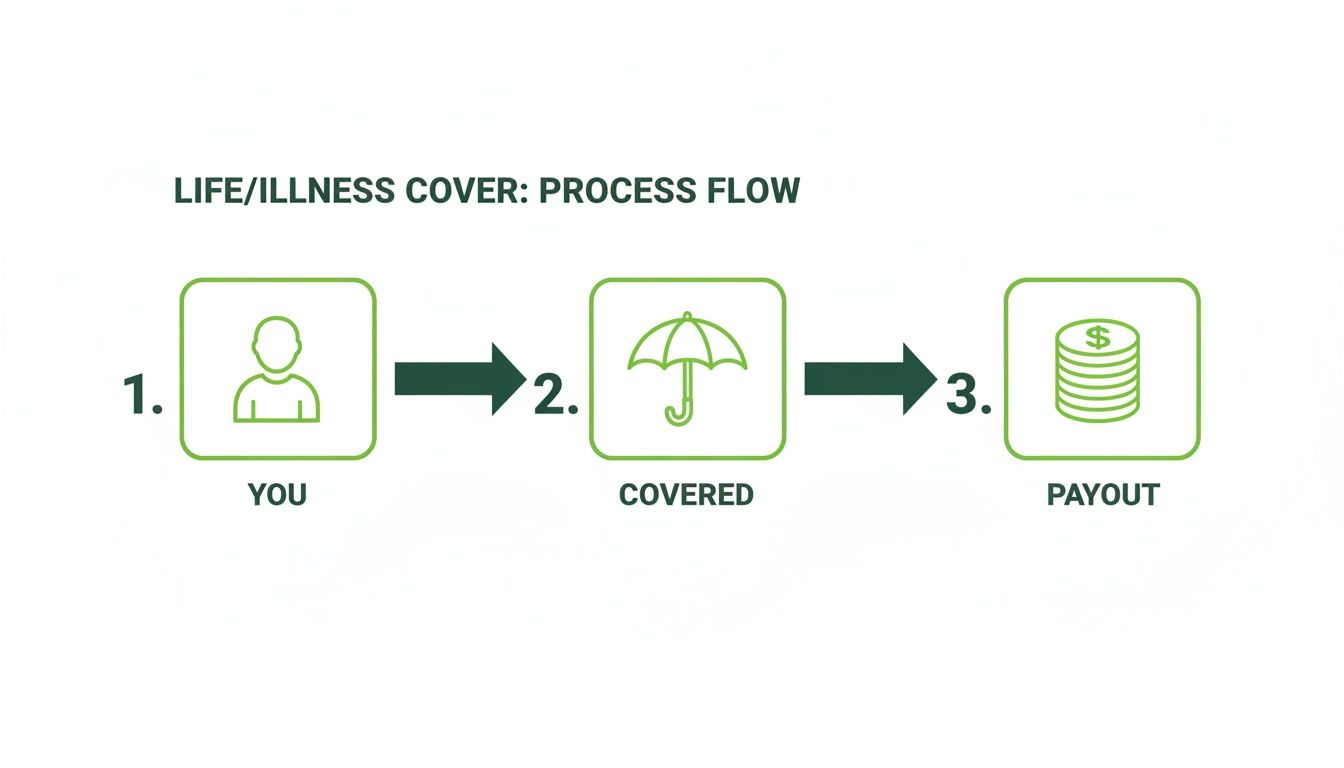

This flowchart breaks down the simple journey from being a policyholder to receiving that crucial payout.

This visual shows the powerful, straightforward purpose of the cover: to provide a financial payout when a specified event happens. It’s a type of protection that more and more people in the UK are turning to. In the first quarter of the year alone, UK protection policies saw 242,418 sales, with premiums totalling over £115 million—a big jump from the previous year. This growth really shows a rising awareness of just how vulnerable families can feel in the face of economic pressures.

The primary goal of a life and critical illness cover payout is to absorb financial shock. It gives families the space to focus on recovery or grieving, free from the immediate pressure of bills and mortgage payments.

This is why it's so important to think not just about short-term protection, but also about how to secure your family's future over the long haul. While term policies are incredibly popular, you might also be interested in exploring our guide on whole of life insurance for more permanent solutions.

When you start looking at life and critical illness cover, you'll quickly realise it isn't a one-size-fits-all product. The best policy is one that’s shaped around your life's unique blueprint—your mortgage, your family's needs, and where you see yourself in 20 years. Getting the structure right is the single most important step.

Think of it like choosing the right tool for a job. You wouldn't use a small hammer to knock down a wall, and the cover you pick needs to be strong enough to handle your specific financial burdens. The good news is that policies are flexible, with a few core types designed to meet the most common needs of families across the UK.

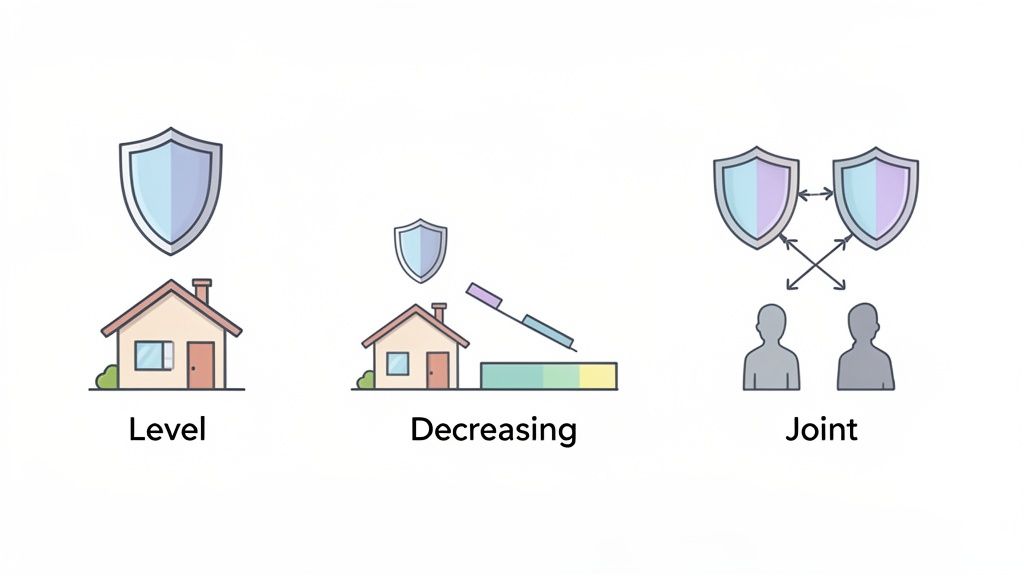

The main choice you'll need to make is whether you want the payout amount to stay the same for the whole policy or shrink over time. Each option has a distinct job to do, aligning with different financial goals. Let's break down the structures you'll come across.

Level term cover is the most straightforward policy you can get. You pick a lump sum amount and a policy length (the ‘term’), and that amount of cover stays completely fixed from day one until the policy ends. If you need to claim, the payout will be the full, original amount you chose.

This consistency makes it the perfect choice for protecting things that don't get smaller over time, like your family's lifestyle or your children's future. If you want to leave enough money to replace your income for the next 20 years, you'll want that amount to be just as substantial in year 15 as it was in year one.

Decreasing term cover is cleverly designed for one main purpose: to protect a repayment mortgage. With this type of policy, the amount of cover reduces over time, roughly in line with your shrinking mortgage balance as you make your monthly payments.

Because the potential payout gets smaller every year, the premiums for decreasing term cover are generally lower than for a level term policy. It’s a really cost-effective way to make sure your single biggest debt is taken care of, freeing your loved ones from that huge financial burden.

If you're in a partnership, you can choose between taking out two separate single policies or one joint policy. A joint life and critical illness cover policy covers both of you but—and this is the crucial part—it only pays out once. After the first valid claim, the policy ends, and the surviving or healthier partner is left with no further cover.

While a joint policy is often a little cheaper than two single ones, this 'first claim' structure is a massive drawback. For this reason, taking out two separate single policies is what we usually recommend. This way, if one partner makes a claim, the other person’s policy remains active, providing continued protection. You can learn more about the nuances by checking out our comprehensive guide on term life insurance and its structures.

The primary goal of a life and critical illness cover payout is to absorb financial shock. It gives families the space to focus on recovery or grieving, free from the immediate pressure of bills and mortgage payments.

Getting your head around the small print of a life and critical illness cover policy can feel a bit intimidating, but it doesn't have to be. The key to real peace of mind is knowing exactly what triggers a payout—and, just as importantly, what doesn't. It's all about setting clear expectations from day one.

At its core, your policy is a list of specific, defined medical conditions. If you're diagnosed with an illness on that list and it meets the insurer's definition for severity, your policy pays out. This clarity ensures that when you need it most, your cover works exactly as you expect.

While every insurer’s list varies a little, most policies are built around a core group of serious illnesses known to have a huge impact on your life and ability to earn a living. You'll find that the "big three" are almost always included, forming a solid foundation for your protection.

These core conditions generally include:

Beyond these, a comprehensive policy will cover a much wider range of conditions. For a deeper dive into the specifics, you can check our dedicated information on critical illness cover. Insurers often provide cover for dozens of illnesses, such as major organ transplants, multiple sclerosis, and kidney failure.

The crucial detail is not just the name of the illness, but the definition used by the insurer. A claim is only successful if your diagnosis matches the specific medical criteria and severity level outlined in your policy documents

For example, a policy might state that a cancer diagnosis is only covered once it has "invaded and spread" and not for "carcinoma in situ," which is a very early-stage cancer. This is why reading and understanding your policy is so vital; it defines the precise circumstances for a payout.

Knowing what isn't covered is just as important as knowing what is. Insurers are very clear about the circumstances where they won't pay a claim, and understanding these from the outset helps you apply with total honesty and manage your expectations.

The most common reasons for a claim being denied tend to fall into a few key areas.

Another critical detail tucked away in your policy is the survival period. This is a standard clause that requires you to survive for a set amount of time after your diagnosis—usually between 10 and 30 days—before the insurer will pay the claim.

This period is in place to distinguish between a critical illness claim and a life insurance claim. If, tragically, you pass away within this window, the life insurance part of your policy would typically pay out to your beneficiaries instead. It’s a simple mechanism to ensure the right part of your combined policy responds to the situation.

Ever wondered why quotes for life and critical illness cover can look so different from one person to the next? It all comes down to a process called underwriting, which is simply the insurer's way of working out how much of a risk you are to insure. They aren't just pulling a number out of thin air; they're carefully calculating the odds of a claim based on your unique circumstances.

Think of it like getting a car insurance quote. A brand-new driver with a souped-up sports car is going to pay a lot more than a seasoned driver with a sensible family hatchback. In the same way, life insurers look at a handful of key factors to build a risk profile that’s specific to you, and that profile directly shapes the monthly premium you’re offered.

Getting your head around these factors is a huge advantage. It puts you in the driving seat and shows you exactly why getting cover sooner rather than later is one of the smartest financial moves you can make to lock in a lower price for good.

When you fill out an application, the insurer will ask a series of questions about your health and lifestyle. Don’t worry, it’s nothing too intrusive. Each answer just helps them build a clearer picture of the risk they’re taking on. These are the main things that will influence your final price.

To bring this to life, imagine a 30-year-old non-smoker in good health who wants £150,000 of cover over 25 years. They’re likely to get a very competitive quote. Now, picture a 45-year-old smoker applying for that same policy. They will face a much higher premium because of the increased risk that comes with both their age and smoking status.

This difference really drives home the value of getting life and critical illness cover sorted early. By locking in a rate while you’re young and healthy, you can secure affordable protection for your family for decades.

Your premium is a direct reflection of your personal risk profile. The lower the perceived risk to the insurer, the lower your monthly cost will be. This makes it crucial to compare offers from different providers, as each may weigh these factors slightly differently.

And you can have confidence that the policy will be there when you need it. The UK’s insurance sector is remarkably stable. The Bank of England’s recent stress test confirmed that UK life insurers maintain exceptional resilience, holding a solvency coverage ratio of 154% even after being hit with simulated, severe financial shocks. This means providers are in a strong position to meet their promises, ensuring your payout is secure. You can learn more about the UK insurance sector's financial strength on bankofengland.co.uk.

Right, so you’ve got your head around the nuts and bolts of life and critical illness cover. That's the first step done. But turning that understanding into real, solid protection for your family is what truly matters.

Getting quotes and finding the right policy can feel like a daunting task, but it’s so much easier when you’ve got an expert in your corner. This is exactly where a good comparison service, connecting you with an FCA-authorised broker, makes all the difference.

A broker acts as your personal guide through the insurance maze. They cut through the jargon, lay out the options from across the market, and make sure your application is spot-on to prevent any headaches down the line. And the best part? This expert guidance doesn't cost you a penny. They work for you, not the insurers, to find the best possible cover at the right price.

Taking cover earlier locks in lower premiums for the duration of the policy.

Getting covered is a straightforward journey from learning to doing. It’s about taking one simple, proactive step that delivers a huge amount of peace of mind. Here’s how you can get the ball rolling and lock in the right policy for you.

An FCA-authorised broker doesn't just find you a price; they find you the right protection. They navigate the complexities of different insurers’ underwriting and policy definitions, ensuring you get cover that truly fits your life.

This process takes all the guesswork and hassle out of it, leaving you free to make a confident, well-informed decision. Comparing life and critical illness cover through a dedicated service is, without a doubt, the smartest way to make sure you’re not overpaying for the protection your family deserves. It’s the final, simple step in turning knowledge into lasting security.

Even after getting to grips with the basics, it’s natural to have a few final questions pop into your head. Let's run through some of the most common queries we hear, giving you the clear, straightforward answers you need to feel confident.

For most people with dependents, absolutely. If you have a partner, children, or a mortgage that relies on your income, it’s one of the smartest financial decisions you can make. For a relatively small monthly cost, it creates a powerful safety net that protects your loved ones from financial turmoil during an already emotional time.

Think of it as buying genuine peace of mind. Knowing your family won't have to worry about the mortgage or bills after a serious diagnosis or your death lets everyone focus on what really matters. Taking out a policy when you’re younger and healthier also means you lock in much cheaper premiums for the long haul.

Yes, in many cases, you can. The golden rule here is to be completely upfront and honest on your application. You must declare every condition you’ve been diagnosed with or treated for, no matter how minor it might seem.

From there, the insurer will take a look at your specific situation. They might:

This is where an FCA-authorised broker is worth their weight in gold. They have deep knowledge of the market and know which insurers are more likely to offer good terms for certain conditions.

This is a really important distinction to understand. A joint policy covers two people but only pays out once—on the very first claim. After that initial payout, whether for a critical illness or a death, the policy simply ends. This leaves the surviving partner with no cover at all.

Two single policies, on the other hand, provide completely independent protection. If one person needs to make a claim, the other person’s policy carries on completely untouched. While two single policies might cost a fraction more, they offer far more comprehensive and robust protection. For this reason, they are almost always the recommended choice for couples.

In the UK, the lump sum payout from a life and critical illness policy is almost always paid tax-free. However, to make sure a life cover payout doesn't accidentally become part of your estate and get hit by Inheritance Tax, you can write the policy 'in trust'. A good broker can help you set this up in minutes.

Ready to protect your family? You can start a free, no-obligation comparison today at Life Cover Plans. Click below to get you're free quote!

Get My Free Quote >>