The real difference boils down to one simple thing: a funeral plan pre-pays for a specific service—the funeral director’s costs—locking in today’s prices. On the other hand, life insurance provides a flexible, tax-free cash lump sum for your loved ones to use however they need.

Your choice really depends on what you want to achieve. Is your priority to guarantee a service is taken care of, or to provide financial breathing room?

Deciding how to cover final expenses is a big step, and the first part of getting it right is understanding what each product is actually designed to do. A funeral plan and a life insurance policy both aim to ease the financial load on your family, but they get there in completely different ways.

This isn't just a small detail; it changes everything—from the cost and flexibility to the kind of peace of mind you're actually buying.

A pre-paid funeral plan is a product you buy to cover the specific costs of a funeral director's services. You're essentially paying for the arrangements in advance, which shields your family from the rising cost of funerals down the line. Once it's paid for, the core services in the plan are guaranteed, no matter how much prices go up.

In contrast, life insurance offers a much broader financial safety net. When you pass away, the policy pays out a fixed, tax-free cash sum to your beneficiaries. Crucially, this money isn't just for the funeral.

The core difference is between a guaranteed service and a versatile cash payout. A funeral plan delivers a pre-arranged funeral, while life insurance delivers capital that can cover the funeral and much more.

This is the key distinction to keep in mind. Think about what your family would find most helpful. Do they need a specific service taken care of, or would a lump sum to manage everything from the funeral to outstanding bills be more useful?

To make things even clearer, this table offers a quick side-by-side summary of the primary features of funeral plans and life insurance. It's a great way to see their core distinctions in a single snapshot.

| Feature | Pre-Paid Funeral Plan | Life Insurance (Whole-of-Life/Over 50s) |

|---|---|---|

| Primary Purpose | To pre-pay for a funeral director's services at today's prices. | To provide a tax-free cash lump sum for beneficiaries to use as needed. |

| Payout Type | A guaranteed service from a chosen funeral director. No cash is paid out. | A fixed cash lump sum paid directly to your beneficiaries. |

| Flexibility | Very low. The plan is tied to specific funeral arrangements. | Very high. Beneficiaries can use the cash for anything (funeral, debts, etc.). |

| Inflation Protection | High. It protects against rising costs for the services included in the plan. | Limited. The cash payout is fixed and may lose value over time. |

| Medical Underwriting | None. Acceptance is guaranteed, regardless of health. | May require medical questions, but Over 50s plans often guarantee acceptance. |

As you can see, they are two very different tools designed for different jobs. A funeral plan is a highly specific solution for a single, predictable cost, whereas life insurance is a flexible financial buffer for a range of potential needs.

The financial engines running a funeral plan and a life insurance policy are worlds apart, and getting to grips with these differences is the key to figuring out which one offers real value for you. This isn't just about the monthly cost; it's about what your money is actually buying—certainty or versatility—and how each product stands up to the ever-present problem of rising costs.

A funeral plan is usually paid for in one of two ways: either a single lump sum upfront or through fixed monthly payments over a set period, like 5, 10, or 20 years. The main draw here is cost certainty. You’re essentially locking in the price of the funeral director's services today, shielding your family from inflation on those specific fees. Once it’s paid, that service is guaranteed.

Life insurance, on the other hand, works on a system of ongoing premiums. For cover like whole-of-life or over 50s plans, you pay a smaller monthly amount for the rest of your life (or until a certain age, say 90). These payments secure a fixed cash payout for your loved ones when you pass away.

When you put the costs side-by-side, the lines can start to blur. A comprehensive funeral plan might cost anywhere from £1,500 for a simple arrangement to £4,500 or more for a more elaborate service.

Let's take an example. A 55-year-old paying for a £4,160 funeral plan over 24 years could find their monthly payments are very similar to someone paying for an over 50s life insurance policy. In fact, data suggests that for this age group, an over 50s policy might cost around £4,288 over the same period, but it provides a flexible cash lump sum, not a fixed service. This makes life insurance a competitively priced alternative that gives your family far more options. You can find out more about how these plans compare in a detailed breakdown from Reassured.co.uk.

The critical difference is what happens if you stop paying. With a funeral plan paid in instalments, you might lose the money you've paid in or only get a partial refund, depending on the provider. With most life insurance policies, your cover simply lapses if you stop paying the premiums.

The core financial trade-off is this: A funeral plan locks in the price of a service, while life insurance secures a cash sum. The plan fights inflation on specific funeral director fees, but the insurance payout's value can be eroded by inflation over time.

This is where the debate between a funeral plan and life insurance becomes crystal clear. The "payout" from a funeral plan isn't cash; it's the delivery of the agreed-upon funeral services by a specific director. There is zero financial flexibility. The money is tied to that one purpose and can't be touched or reallocated by your family.

A life insurance payout is the complete opposite. It’s a tax-free cash lump sum paid directly to your beneficiaries, giving them total control over how it’s used.

This flexibility is a huge advantage, especially as family needs can change in unpredictable ways over the years. A cash sum is a responsive solution to whatever financial challenges your loved ones might be facing. While a pre-paid service is helpful, it only solves one specific problem.

The structure of these products also impacts your long-term financial planning. A funeral plan is a finite commitment; once you've paid it off, it’s done and dusted. This can be appealing for those who want to settle the cost and forget about it. However, it's an inflexible asset once it's in place.

Life insurance policies, including the simpler term life insurance policies that cover you for a set period, offer much more adaptability. The fixed cash payout from a whole-of-life or over 50s policy gives your family the power to adapt to the economic realities at the time of your death—a powerful form of protection in itself.

Before weighing up a funeral plan against life insurance, it’s vital to get a real sense of the financial pressure your family could be facing. The cost of a funeral in the UK isn't a fixed number; it's a rapidly climbing expense that has been outpacing general inflation for years. It’s a trend that makes planning ahead more important than ever.

For too many families, the final bill comes as a huge shock, landing at a time when they’re already emotionally shattered. Without a plan in place, these soaring costs can easily lead to debt, stress, and painful compromises on how a loved one is remembered.

The financial reality of arranging a funeral has changed beyond recognition over the last couple of decades. What used to be a manageable expense is now a major financial event, one that can place a heavy burden on the people you leave behind. And this isn't a small jump; the numbers show a steep and relentless climb.

In fact, data shows the average cost of a basic funeral has more than doubled since 2004. This trend really highlights how traditional savings can struggle to keep up. For instance, the latest figures reveal the average total cost of dying in the UK has now hit £9,263—a staggering 126% increase over a 20-year period. This sharp rise underscores the urgent need for a dedicated financial solution.

The key takeaway here is that simply putting money aside might not be enough. With costs rising so fast, your savings can easily fall short, leaving your family to unexpectedly cover the difference.

The final bill is heavily influenced by the choices made, especially between a burial and a cremation. Seeing the real-world figures gives a much clearer picture of the financial challenge your loved ones could face.

These figures from SunLife's 2024 Cost of Dying Report paint a very clear picture. Even the most basic arrangements come with a four-figure price tag, reinforcing why having a proper plan is so necessary.

The trend of rising funeral costs shows no sign of slowing down. Projections based on the current growth rates are a real cause for concern and add another layer of urgency to the decision between a funeral plan and life insurance.

If costs keep climbing at this pace, the average funeral could set you back £6,733 by 2034. That’s a potential 43% increase from where we are today. This future financial pressure is exactly what products like funeral plans and life insurance are designed to solve.

A funeral plan aims to lock in the price of the director's services right now, protecting you directly from this inflation. Life insurance provides a cash lump sum that’s intended to be large enough to cover these future costs and more. Both are a direct response to the same problem: the certainty of rising expenses. Getting to grips with the scale of this problem is the first step in choosing the right solution for your family.

Knowing the features of a funeral plan versus life insurance is one thing, but seeing how they work in the real world is where it all clicks. The best choice often has less to do with the product itself and more to do with your own life, your financial commitments, and what you really want to achieve for your family.

To make this crystal clear, let's walk through three common scenarios that most families in the UK will recognise. By looking at the main goal in each situation, we can see which option offers the most sensible and effective solution.

Let’s meet Sarah and Tom. They're in their early 40s, have a hefty mortgage on their home, and two children under the age of ten. Their biggest financial worry isn't just the cost of a funeral; it's making sure the family can keep living in their home and maintain their lifestyle if one of them were to pass away.

Their main goal is comprehensive financial protection. They need something that can clear the mortgage, replace a lost income, and help with future costs like university fees, on top of any final expenses.

In this case, term life insurance is the clear winner. A funeral plan would only sort out the funeral director's services, leaving the biggest financial headaches—the mortgage and childcare costs—untouched. A term life policy, on the other hand, can be set up to deliver a substantial, tax-free cash payout that would wipe out the mortgage and give the surviving partner a vital financial cushion.

For young families with major debts like a mortgage, the flexibility and scale of a life insurance payout offer a level of security that a funeral plan simply cannot match. It addresses the entire financial picture, not just one specific cost.

Now, let's think about David and Linda, who are in their late 50s. Their mortgage is gone, and their kids are grown up and financially independent. They've got savings and pensions sorted for their retirement, but they want to make sure their children aren't hit with a sudden bill for their funerals. They also like the idea of leaving a little cash gift behind.

Their main goal is to provide a straightforward, flexible legacy to cover final expenses and leave something extra for their children or grandchildren, without the hassle or medical checks of some traditional life insurance policies.

This is the perfect spot for an over-50s life insurance plan. These policies guarantee acceptance for UK residents aged 50-85 with no medical questions, which makes them incredibly easy to set up. The fixed cash payout would give their children the freedom to arrange a fitting funeral and use any leftover money as they wished—maybe for a family holiday in their memory or to put towards their own savings. A funeral plan would feel too rigid here, locking them into a specific service when their children might prefer to handle the arrangements themselves.

If this situation sounds familiar, it's worth taking a closer look at guaranteed over 50s life insurance plans to see how they deliver both peace of mind and flexibility.

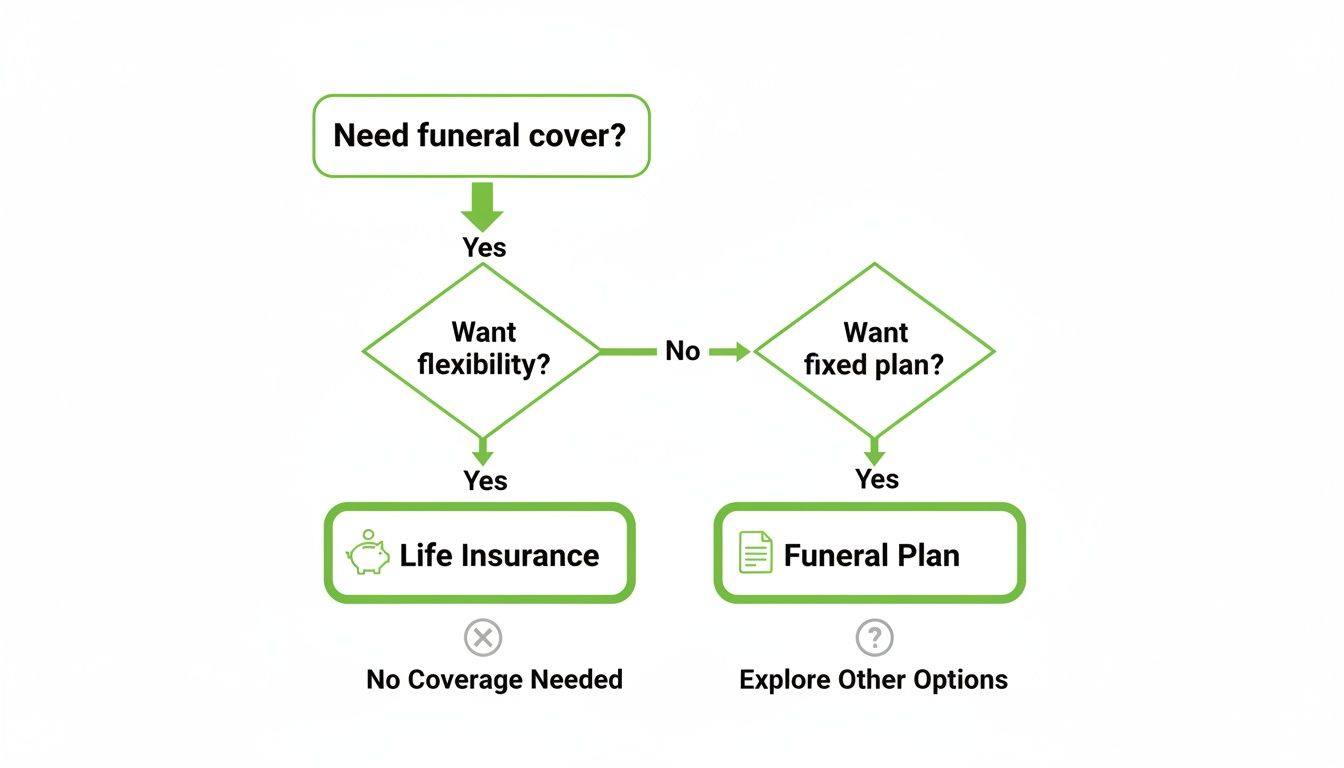

This simple decision tree can help you quickly see which path might be right for your needs, based on whether you're focused on a pre-set service or financial flexibility.

The flowchart shows that the fundamental choice in the funeral plan vs life insurance debate comes down to your desire for control and flexibility versus a pre-set arrangement.

Finally, let's look at Margaret, a 72-year-old single woman. She has no big debts and lives a quiet life. Her main concern is that her specific funeral wishes—a particular type of service, certain music, and cremation—are carried out exactly as she wants them, without causing any organisational or financial stress for her relatives who live far away.

Her primary goal is absolute certainty and removing all decision-making burdens from her family. She isn't worried about leaving a flexible cash sum; she wants a specific job taken care of.

For Margaret, a pre-paid funeral plan is the ideal solution. It lets her plan every detail in advance and lock in the price of the funeral director's services at today's rates. When the time comes, her relatives just have to make one phone call to the plan provider, and everything she arranged will be put into motion. Life insurance wouldn't work for her, as it would put the job of arranging and paying for the funeral right back on her relatives' shoulders—the very thing she wants to avoid.

As these scenarios show, there’s no single "best" product. The right choice in the funeral plan vs life insurance debate is always the one that fits your stage of life, your financial responsibilities, and the kind of support you want to leave behind.

When you’re weighing up a funeral plan against life insurance, it’s easy to get stuck thinking it has to be one or the other. The reality for most UK households, though, is a lot messier. Families often end up pulling money from several different places to cover the final bill, mixing formal plans with personal savings just to manage the cost.

Understanding how people actually pay for funerals teaches us a crucial lesson: it's rarely about a single product. It’s about creating a layered financial safety net. By looking at how things work in the real world, we can see what’s common, where the pitfalls are, and how you can build a smarter, more resilient plan for your own family.

The way people cover final expenses is a real patchwork of different products and assets. The data shows that families don’t just rely on one neat solution, but a combination of pre-arranged plans, insurance policies, and whatever they can find in personal accounts.

When it comes to paying for a funeral, 33% of people use a pre-paid funeral plan, which makes sense for anyone wanting to lock in specific services. At the same time, a combined 22% turn to life insurance, split evenly between standard life cover and specialist over-50s plans. But these formal products are often just part of the story. A huge 23% use savings and investments, and another 16% have to dip into current accounts. This highlights a key trend: many households end up cobbling together funds from various pots to meet the final cost. You can explore the full breakdown in the SunLife Cost of Dying Report.

The critical takeaway here is that a huge number of families are under-protected. Research shows that while roughly 70% of people have made some kind of provision, only 42% have enough tucked away to cover the actual costs, creating a major protection gap.

This shortfall means that even with a plan in place, families can still be hit with unexpected bills, adding financial stress at the worst possible time. It really hammers home the importance of not just having a plan, but making sure it provides enough cover for realistic, modern-day costs.

That gap between what people have saved or insured and the final funeral bill is a massive problem. This shortfall often happens because the product chosen—whether it's a small over-50s policy or a basic funeral plan—simply doesn't account for all the extra expenses that crop up.

Several things contribute to this financial gap:

This reality is exactly why a single-product approach can be so risky. Relying only on a basic funeral plan might leave your family exposed to rising third-party fees, while a small life insurance policy might not keep up with inflation.

The most effective way to protect your loved ones is by thinking beyond the binary choice of a funeral plan vs life insurance. Smart planning often involves using these products together, letting them cover different bases to create a complete financial shield.

For example, someone might take out a pre-paid funeral plan to lock in the director's services and ensure their specific wishes are met. Alongside this, they could hold an over-50s life insurance policy to provide a flexible cash lump sum. This cash can then be used by their family to cover those unpredictable third-party costs, pay for the wake, settle any small outstanding bills, or just provide a comforting financial buffer during a tough time.

This layered approach deals with both the need for certainty and the need for flexibility. It effectively closes the protection gap and ensures total peace of mind.

Choosing between a funeral plan and life insurance really boils down to what you’re trying to achieve. A funeral plan is a specialist tool for one job: locking in the price of a funeral director's services. But for most people looking for real financial flexibility and a robust safety net for their family, life insurance offers far more value.

A life insurance payout provides a tax-free cash lump sum, which puts your loved ones in control. They can use it to cover funeral costs, yes, but also to pay off the mortgage, clear outstanding debts, and simply manage day-to-day living expenses without immediate financial panic. That versatility is a massive advantage when facing an uncertain future.

Finding the right policy doesn't have to be a headache. Our free, no-obligation comparison service is designed to cut through the noise, helping you secure the ideal cover from the UK’s leading insurers. We’ll help you quickly see how the different types of policies stack up for your needs and budget.

By comparing quotes, you ensure you're not overpaying for your premiums. Our service connects you with FCA-authorised brokers who can provide tailored options without any pressure.

Taking a few moments to compare policies is the single most effective step you can take towards securing affordable, reliable financial protection. It’s about getting the peace of mind that comes from knowing your loved ones will be looked after, no matter what.

When you're weighing up your options, it's natural for a few specific questions to pop up. Let's run through some of the most common ones we hear when people are comparing funeral plans against life insurance, giving you the clear answers you need.

Yes, you absolutely can. In fact, for a lot of people, it’s a really smart strategy. The two products are built for different jobs, and having both can create a far more robust financial safety net for your loved ones.

Think of it this way: the funeral plan can lock in the director's costs and handle the practical side of the arrangements, taking that burden away from your family. Meanwhile, the life insurance policy provides a flexible, tax-free cash sum. This money can then be used to cover any third-party funeral costs not included in the plan (like cremation fees or flowers), clear outstanding bills, or simply give your family some financial breathing room. It’s a combined approach that ticks both the practical and financial boxes.

This is a really important question, and it highlights one of the biggest drawbacks of a funeral plan. They can be surprisingly restrictive. If your plan is tied to a specific funeral director and you end up moving to another part of the country, transferring it might not be simple.

Some providers will sting you with an administration fee, while others might not even have a participating director in your new area, potentially forcing you to cancel the plan altogether. Life insurance completely sidesteps this problem. Because it pays out cash, your beneficiaries have total freedom to choose any funeral director they want, anywhere in the UK, when the time comes.

A funeral plan's lack of portability can be a real issue. Life insurance gives your family complete geographic freedom, as the cash payout can be used with any service provider they choose, regardless of where they live.

The consequences of stopping your payments are drastically different for each product, and it's something you need to be crystal clear on.

It's crucial to get your head around these terms before you commit. The risk of losing your investment is a major point of difference in the funeral plan vs life insurance debate.

At Life Cover Plans, we make finding the right financial protection for your family straightforward. You can compare free, no-obligation quotes from the UK's top insurers in minutes and get the peace of mind you deserve. Click below to get your free quote now!

Get My Free Quote >>