At first glance, Critical Illness Cover and Income Protection can seem quite similar. Both are designed to provide a financial lifeline if your health takes a turn for the worse. But dig a little deeper, and you’ll find they are built to solve entirely different problems.

The key difference is simple: Critical Illness Cover pays you a one-off, tax-free lump sum if you’re diagnosed with a specific serious condition listed in your policy. On the other hand, Income Protection provides a regular, tax-free monthly income if any illness or injury stops you from being able to work.

Think of it like this: one is a financial sledgehammer, the other is a replacement for your monthly paycheque.

When you’re planning how to protect your finances, getting your head around the distinction between these two types of cover is essential. While both offer a safety net, they step in at different times and in very different ways.

Critical Illness Cover is all about tackling the immediate, and often huge, financial burdens that can come with a serious diagnosis. The lump sum payout gives you complete flexibility to use the money however you see fit.

You could use it to:

Income Protection is designed for long-term stability. It’s not tied to a specific list of illnesses; it pays out if any medically certified illness or injury prevents you from doing your job.

This cover acts as a direct replacement for a portion of your salary. It ensures you can continue to meet all your regular monthly commitments—like mortgage or rent payments, utility bills, and the weekly food shop—if you’re unable to work for an extended period.

To make the comparison crystal clear, let's break down their core functions side-by-side.

Here’s a simple table to help you quickly see how these two policies stack up against each other.

| Feature | Critical Illness Cover | Income Protection Insurance |

|---|---|---|

| Payout Type | A one-off, tax-free lump sum payment. | Regular, tax-free monthly payments. |

| Claim Trigger | Diagnosis of a specific, pre-defined serious illness (e.g., cancer, stroke). | Inability to work due to any illness or injury, confirmed by a doctor. |

| Primary Purpose | Covers large, immediate costs like clearing a mortgage or medical bills. | Replaces lost earnings to cover ongoing, day-to-day living expenses. |

| Coverage Scope | Limited to the specific list of conditions defined in your policy. | Covers any medical condition that prevents you from working. |

Ultimately, choosing between them—or deciding if you need both—comes down to your personal circumstances, your financial obligations, and the kind of peace of mind you’re looking for.

Critical Illness Cover is a very specific type of protection. It’s designed to do one job: deliver a single, tax-free lump sum of cash if you’re diagnosed with a serious medical condition that’s listed in your policy.

This is the key difference when you compare it to income protection. The payout is triggered purely by the diagnosis itself, not by whether you’re physically able to work. In fact, you could be diagnosed with a covered illness, continue working, and still receive the full cash payout.

The whole point of this lump sum is to provide powerful and immediate financial relief at one of the most difficult times imaginable. It gives you the freedom to tackle major financial pressures head-on, so you can focus all your energy on your health and recovery.

Families often use this money for life-changing financial moves, such as:

A critical illness diagnosis can bring unexpected and significant costs. The lump-sum payout is designed to act as a powerful financial tool, giving you complete control over how to manage these new challenges without liquidating savings or going into debt.

The real-world impact of these policies is huge. For instance, recent data from Aviva shows it paid out £362 million across 5,048 critical illness claims in 2024 alone, with an average payout of £71,833. This just goes to show the vital role this cover plays in providing a financial cushion when a crisis hits.

The exact list of illnesses covered will vary between insurers, but most policies will include the most common and serious conditions that affect people here in the UK. When you compare critical illness life insurance quotes, it's absolutely essential to read the policy definitions carefully.

Typically, you can expect a policy to cover:

The more comprehensive policies can cover dozens of conditions, from major organ transplants and kidney failure to permanent paralysis. Some may also offer smaller, partial payments for less severe conditions, giving you a degree of financial help without ending the full policy.

Because the payout is tied to a specific list of illnesses, understanding what is and isn't covered is the most important part of choosing a policy. This is where the debate of critical illness vs income protection becomes crystal clear: one covers a defined list of events, while the other covers your ability to earn an income.

While critical illness cover gives you a one-off financial boost, Income Protection works in a completely different way. Think of it as your financial stand-in, stepping in to replace your regular salary when you physically can't earn it yourself.

This policy pays out a regular, tax-free monthly income if any illness or injury stops you from working. This is a crucial difference in the critical illness vs income protection debate. The trigger isn't a specific diagnosis from an insurer's list; it’s simply your inability to do your job, confirmed by a doctor.

The whole point of income protection is to keep your finances stable over the long haul. Those monthly payments make sure you can keep on top of your regular commitments without having to raid your savings or get into debt.

These regular payments are designed to cover all the essential outgoings:

And these policies really do deliver. Take MetLife UK, a major provider in this space. They paid out an incredible £34 million across 31,553 accident and sickness claims in 2025 alone. With a 94% payout rate, it shows just how vital this support is for UK families. You can read more about it in the latest MetLife UK claims report.

When you set up an income protection policy, you get to control a few key features that directly affect your premiums and how the cover works. One of the most important is the deferred period.

The deferred period is simply the waiting time you agree to between stopping work and the policy starting to pay you. This can be anything from four weeks up to a year.

The longer your deferred period, the lower your monthly premiums will be. A smart move is to line this up with your employer's sick pay policy or how long your own savings could tide you over, creating a seamless financial bridge.

Another critical choice is your level of cover. You can usually insure between 50% and 70% of your gross monthly income. This is set at a level to replace your take-home pay, letting you maintain your lifestyle while you focus on recovery. The policy keeps paying out until you can go back to work, the policy term ends, or you retire—whichever comes first.

This structure makes income protection a powerful safety net against a huge range of health problems, from a serious back injury to mental health conditions that make work impossible.

To really get to the heart of the critical illness vs income protection debate, we need to look past the simple definitions. Yes, one pays a lump sum and the other a monthly income, but how they work on a day-to-day level is fundamentally different. These distinctions are what will ultimately tell you which policy is the right fit for the specific financial holes you’re trying to fill.

Let's break down the four most important differences: what triggers a payout, how the money is paid, the range of illnesses covered, and how long the policy typically lasts. Each one shows you the unique job these policies are built to do.

The single biggest difference between these two types of cover is what actually has to happen for you to get paid. This trigger event is what starts a claim, and they are worlds apart.

Critical Illness Cover is all about a specific diagnosis. Your policy will have a very precise list of medical conditions and exactly how severe they need to be to qualify for a payout. It’s not enough to be told you have "cancer"; it usually has to be a cancer of a defined type and stage. You could get your diagnosis, receive the full lump sum, and even be back at work a few weeks later.

Income Protection, on the other hand, is triggered by your inability to work. It doesn't care what illness or injury you have—it could be a bad back, severe stress, or something not listed on any critical illness policy. If a doctor signs you off as medically unfit to do your job, the policy is designed to kick in and start paying out after your chosen waiting period.

Key Takeaway: Critical Illness Cover is about the what—the specific diagnosis you've received. Income Protection is about the effect—the fact you can't earn an income, whatever the reason. This is the absolute core of the critical illness vs income protection comparison.

This structural difference is vital. A lump sum is incredibly powerful but it's also finite. In contrast, a monthly income provides ongoing, reliable support that can last for years, or even right up until you retire.

The range of conditions each policy covers also varies massively, which has a direct impact on how likely you are to be able to make a successful claim.

A Critical Illness policy is, by its very nature, limited. It only covers the specific conditions named in the policy document. While these are usually the most severe illnesses like heart attacks, strokes, and advanced cancers, if your condition isn't on that list, you're not covered. Simple as that.

In stark contrast, Income Protection offers far broader protection. Because its focus is on your ability to work, it can cover a huge range of medical issues. In fact, official statistics consistently show that musculoskeletal problems (like back pain) and mental health conditions are two of the biggest reasons for long-term absence from work in the UK. Neither would typically trigger a critical illness payout, but both are very common reasons for a successful income protection claim.

Finally, the typical length or "term" of each policy tends to line up with completely different financial goals.

Critical Illness Cover is very often set up to run for the same length of time as a mortgage. The logic is simple and powerful: if a serious illness hits, the lump sum can wipe out the home loan, removing the family's single biggest monthly expense. A 25-year policy term is the perfect partner for a 25-year mortgage.

Income Protection, however, is designed to protect your most valuable asset—your ability to earn—for your entire working life. Because of this, it's usually set up to run until your planned retirement age, say 65 or 68. This guarantees your income is protected right up to the day you expect to start drawing your pension.

To see these differences side-by-side, it helps to put them in a table. This format cuts through the noise and lets you directly compare the core features of each policy, making it easier to see which one aligns with your personal protection needs.

| Comparison Point | Critical Illness Cover | Income Protection Insurance |

|---|---|---|

| Main Purpose | To clear large debts or cover one-off costs after a specific serious diagnosis. | To replace your regular monthly income if any illness or injury stops you from working. |

| Payout Trigger | Diagnosis of a specific illness listed in the policy to a defined severity. | Being medically signed off work by a doctor, regardless of the condition. |

| Payout Format | A single, tax-free lump sum payment. | A regular, tax-free monthly income, like a replacement salary. |

| Coverage Scope | Limited to a defined list of serious conditions (e.g., cancer, heart attack, stroke). | Covers almost any illness or injury that prevents you from working. |

| Common Exclusions | Conditions not on the list, or those not meeting the required severity. | Pre-existing conditions may be excluded, as well as self-inflicted injuries. |

| Typical Policy Term | Often matched to a mortgage term (e.g., 25 years). | Usually set to run until your planned retirement age (e.g., 65 or 68). |

| Best For... | Protecting against the financial impact of a life-changing diagnosis. Ideal for homeowners. | Protecting your day-to-day lifestyle and meeting ongoing financial commitments. |

As you can see, they are not interchangeable. They are two distinct tools designed for two very different jobs, and understanding this is the first step toward building a financial safety net that truly works for you.

Understanding the technical details is one thing, but seeing how these policies actually perform in real life is what truly makes sense of them. The abstract ideas of lump sums and monthly incomes become much clearer when you apply them to situations that families across the UK face every day. These stories really highlight the specific financial problems each type of policy is designed to fix.

To show you what I mean, let’s walk through three different scenarios. Each one shows how a different protection strategy can provide crucial support during a health crisis, helping you picture which approach might be the right fit for you.

Meet Sarah, a 42-year-old marketing manager and homeowner. Sarah has a £225,000 mortgage and, when she bought her house, she wisely took out a critical illness policy for the same amount. Her biggest financial worry was making sure that huge debt would be wiped out if she ever got a serious diagnosis, taking that enormous monthly pressure off her family.

Last year, Sarah was diagnosed with a type of cancer covered by her policy. Once her diagnosis was confirmed and the insurer approved the claim, she received a £225,000 tax-free lump sum. She used the entire amount to pay off her mortgage in full. That single action immediately freed up over £1,200 a month in her household budget, giving her the breathing room to cut back her work hours and focus completely on her treatment without the fear of losing her home. Our guide on how life insurance can protect your mortgage explores this strategy in more detail.

Now let’s look at Mark, a 35-year-old self-employed graphic designer. As a freelancer, Mark gets no sick pay from an employer, so any time off work means his income stops dead. His biggest concern wasn't a specific illness, but any health issue that could stop him from working for months on end.

Mark chose an income protection policy that would pay him £2,500 a month after a three-month waiting period. After a severe back injury from a fall left him unable to sit at his desk, his policy kicked in. For the seven months he couldn't work, those regular payments covered his rent, bills, and groceries. The policy acted as his replacement salary, ensuring life could carry on without him having to drain his savings or go back to work before he was medically ready.

The crucial difference here is that Mark's back injury would not have triggered a critical illness payout. His income protection policy was the exact safety net he needed for a common but debilitating condition that simply stopped him from earning a living.

Finally, let's consider David, a 55-year-old engineer with a family. Understanding the different risks he faced, David decided he needed both types of cover. He had a £100,000 critical illness policy and an income protection policy that would pay out £3,000 a month right up until his planned retirement age.

When David suffered a major stroke, both of his policies were triggered. He received the £100,000 lump sum from his critical illness cover almost immediately. His family put this money to work on urgent needs: paying for private physiotherapy to speed up his recovery, adapting their home to be wheelchair accessible, and covering his partner’s unpaid leave from work.

At the same time, after his three-month deferred period ended, his income protection policy started paying him £3,000 every single month. This ongoing income made sure all the regular family bills were paid throughout his lengthy, year-long recovery. This two-policy approach shows how the covers can work in tandem, with one tackling the immediate, large costs and the other providing long-term stability. Recent market analysis highlights this trend, showing a significant rise in critical illness uptake among those aged 35-54, who are increasingly aware of the financial shock of a major diagnosis. Learn more about these critical illness insurance statistics and market trends.

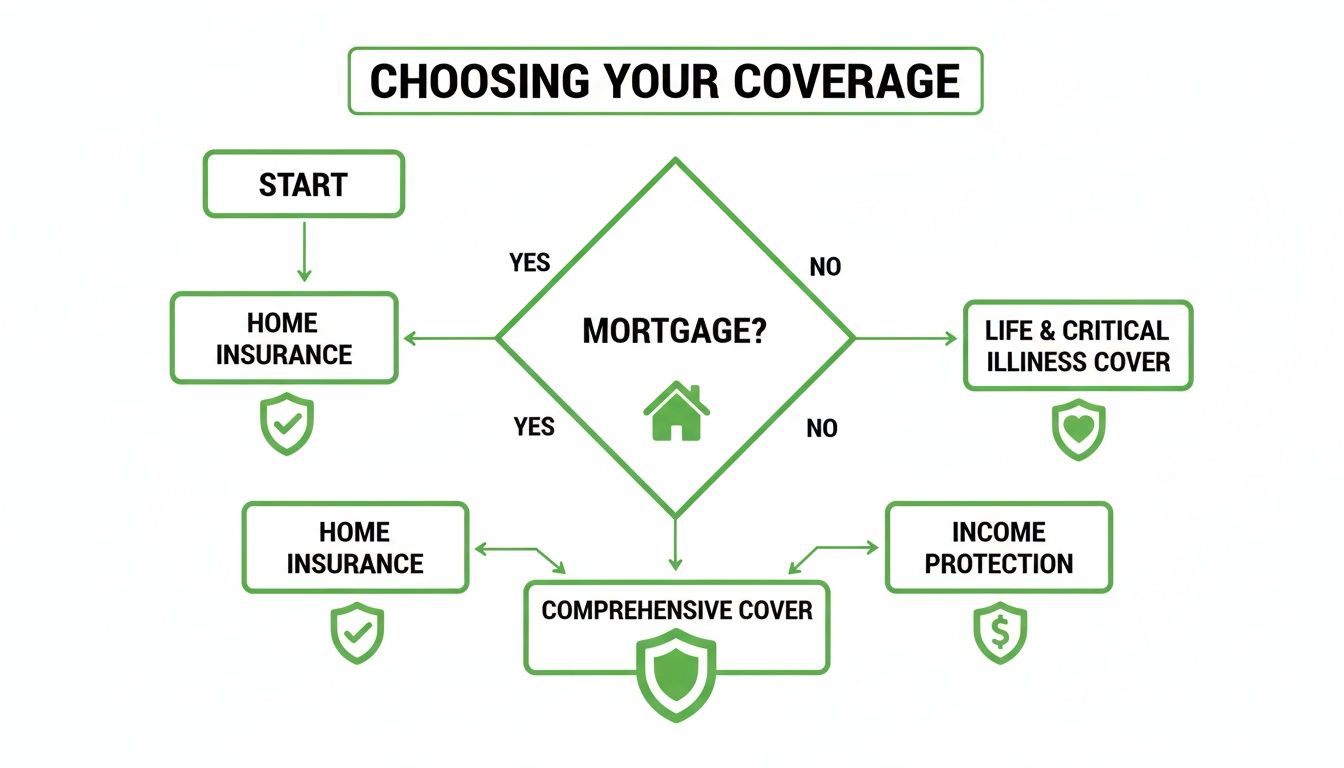

So, Critical Illness Cover or Income Protection? It's a common dilemma, and the right answer really boils down to one simple question: what’s the biggest financial hole you need to plug?

While having both policies would create the ultimate financial safety net, most of us have to make a choice based on our budget. The key is to take a hard look at your own circumstances and figure out where you’re most vulnerable. It's a personal decision, but there's a clear way to approach it.

Start with your debts and your savings. If you have a hefty mortgage or other large loans hanging over you, securing a way to wipe them out in one go might be your top priority. On the other hand, if your savings account is looking a bit thin, making sure your monthly bills get paid is probably the more urgent concern.

This decision-tree flowchart can help you visualise the thought process and guide you towards the right type of cover for your situation.

As you can see, your biggest financial commitments—whether it's the mortgage or a lack of emergency funds—are what point you in the right direction.

When comparing critical illness vs income protection, think of it this way: one is a shield for your biggest assets (like your home), while the other is a replacement for your most valuable asset—your ability to earn an income.

Before you commit to a policy, it’s always worth checking what your employer offers. Some companies provide a generous sick pay scheme that might cover your salary for several months. If that’s the case, you could choose an income protection policy with a longer waiting period before it pays out, which can significantly lower your monthly premiums.

But a word of caution: employer benefits are rarely a complete, long-term solution. They might not pay out for the entire duration of a serious illness, and crucially, they are tied to your job. If you switch employers, you could lose that cover overnight. A personal policy gives you security that stays with you, no matter where you work. At the end of the day, your personal situation—your debts, your savings, and any existing cover—is what should guide your decision.

You've done the hard part – getting your head around the difference between Critical Illness Cover and Income Protection. But knowing the theory is one thing; turning it into a real financial safety net for your family is what truly matters.

The honest answer is there's no "best" policy that works for everyone. The right choice is completely personal. It depends on everything from the size of your mortgage and your savings buffer to whether you have kids who rely on you.

While it might feel like a big decision, the next step is actually quite simple. The best way forward is to see what real policies look like for you. Comparing quotes from a few trusted UK insurers lets you weigh up the actual costs and see the features side-by-side.

It’s the quickest way to move from abstract ideas to concrete numbers.

Comparing quotes is a great start, but the small print in insurance policies can be tricky. This is where getting a bit of expert advice really pays off. Speaking with an FCA-authorised broker gives you the confidence that you're making the right call. They'll look at your specific situation and give you straightforward recommendations, making sure you don't end up paying for cover you don't need or missing a crucial detail.

A good broker can help you nail down the important decisions, like:

The whole point is to build a financial safety net that fits your life like a glove. Getting proper guidance ensures the protection you choose is robust enough to actually work when you need it most.

Putting this all into action is easier than you think. Using a free comparison service takes all the hassle out of it, putting you in touch with specialists who can give you the quotes and advice you need.

This approach takes the guesswork out of the equation and lets you make a properly informed decision. By taking just a few minutes to compare your options, you're taking a huge step towards securing your family's financial future. Explore your options and get your free life insurance quotes today to find the right protection for your peace of mind.

Ready to compare quotes? At Life Cover Plans, we make it easy to find affordable cover from the UK's leading insurers. Click below to get your free no-obligation quote and secure your family’s future in minutes.

Get My Free Quote >>